Yahoo Finance

Yahoo Finance We're Hopeful That Natural Gas Services Group (NYSE:NGS) Will Use Its Cash Wisely

Just because a business does not make any money, does not mean that the stock will go down. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

So, the natural question for Natural Gas Services Group (NYSE:NGS) shareholders is whether they should be concerned by its rate of cash burn. For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). Let's start with an examination of the business' cash, relative to its cash burn.

See our latest analysis for Natural Gas Services Group

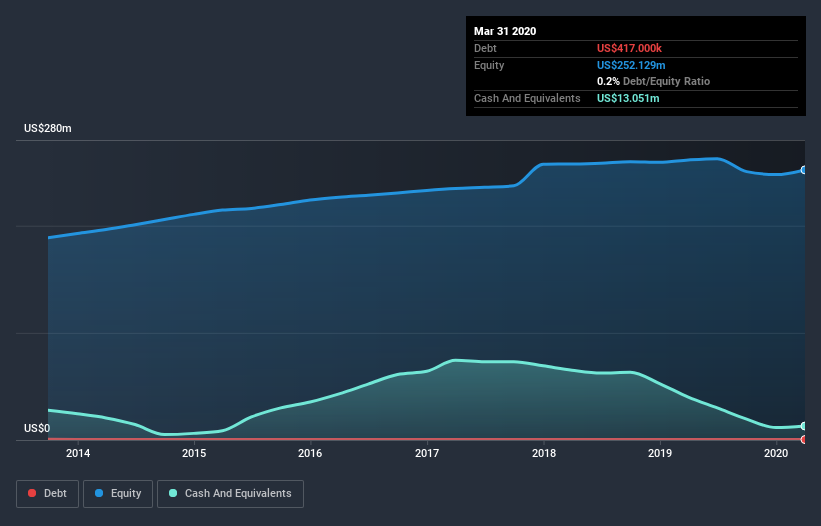

Does Natural Gas Services Group Have A Long Cash Runway?

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at March 2020, Natural Gas Services Group had cash of US$13m and such minimal debt that we can ignore it for the purposes of this analysis. Importantly, its cash burn was US$26m over the trailing twelve months. So it had a cash runway of approximately 6 months from March 2020. Importantly, though, analysts think that Natural Gas Services Group will reach cashflow breakeven before then. If that happens, then the length of its cash runway, today, would become a moot point. The image below shows how its cash balance has been changing over the last few years.

How Well Is Natural Gas Services Group Growing?

In the last twelve months, Natural Gas Services Group kept its cash burn steady. And while its operating revenue growth of 14% didn't shoot the lights out, it does, at least, point to business traction. Considering the factors above, the company doesn’t fare badly when it comes to assessing how it is changing over time. While the past is always worth studying, it is the future that matters most of all. So you might want to take a peek at how much the company is expected to grow in the next few years.

How Hard Would It Be For Natural Gas Services Group To Raise More Cash For Growth?

Given the trajectory of Natural Gas Services Group's cash burn, many investors will already be thinking about how it might raise more cash in the future. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Many companies end up issuing new shares to fund future growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Since it has a market capitalisation of US$89m, Natural Gas Services Group's US$26m in cash burn equates to about 29% of its market value. That's not insignificant, and if the company had to sell enough shares to fund another year's growth at the current share price, you'd likely witness fairly costly dilution.

Is Natural Gas Services Group's Cash Burn A Worry?

Even though its cash runway makes us a little nervous, we are compelled to mention that we thought Natural Gas Services Group's revenue growth was relatively promising. It's clearly very positive to see that analysts are forecasting the company will break even fairly soon. While we're the kind of investors who are always a bit concerned about the risks involved with cash burning companies, the metrics we have discussed in this article leave us relatively comfortable about Natural Gas Services Group's situation. Readers need to have a sound understanding of business risks before investing in a stock, and we've spotted 1 warning sign for Natural Gas Services Group that potential shareholders should take into account before putting money into a stock.

Of course Natural Gas Services Group may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.