Yahoo Finance

Yahoo Finance WalkMe's (NASDAQ:WKME) Q1 Earnings Results: Revenue In Line With Expectations

User support software provider WalkMe (NASDAQ: WKME) reported results in line with analysts' expectations in Q1 CY2024, with revenue up 4.1% year on year to $68.57 million. The company expects next quarter's revenue to be around $69.5 million, in line with analysts' estimates. It made a non-GAAP profit of $0.07 per share, improving from its loss of $0.08 per share in the same quarter last year.

Is now the time to buy WalkMe? Find out in our full research report.

WalkMe (WKME) Q1 CY2024 Highlights:

Revenue: $68.57 million vs analyst estimates of $68.11 million (small beat)

Operating profit (non-GAAP): $4.4 million vs analyst estimates of $1.1 million (beat)

EPS (non-GAAP): $0.07 vs analyst estimates of $0.02 ($0.05 beat)

Revenue Guidance for Q2 CY2024 is $69.5 million at the midpoint, roughly in line with what analysts were expecting

The company reconfirmed its revenue guidance for the full year of $281 million at the midpoint

The company raised its operating profit (non-GAAP) guidance for the full year of $13.8 million at the midpoint (above estimates)

Gross Margin (GAAP): 85.6%, up from 81.5% in the same quarter last year

Free Cash Flow of $16.64 million, up 99.1% from the previous quarter

Market Capitalization: $718.9 million

“Q1 has been a great kickoff as we turn the corner on growth with a focus on doubling our net new ARR in 2024,” said Dan Adika, CEO of WalkMe.

Founded in Israel in 2011, WalkMe (NASDAQ:WKME) is software that teaches users how to get the most out of new applications.

Customer Support

Companies need to be able to interact with and sell to their customers as efficiently as possible. This reality coupled with the ongoing migration of enterprises to the cloud drives demand for cloud-based customer relationship management (CRM) software that integrates data analytics with sales and marketing functions.

Sales Growth

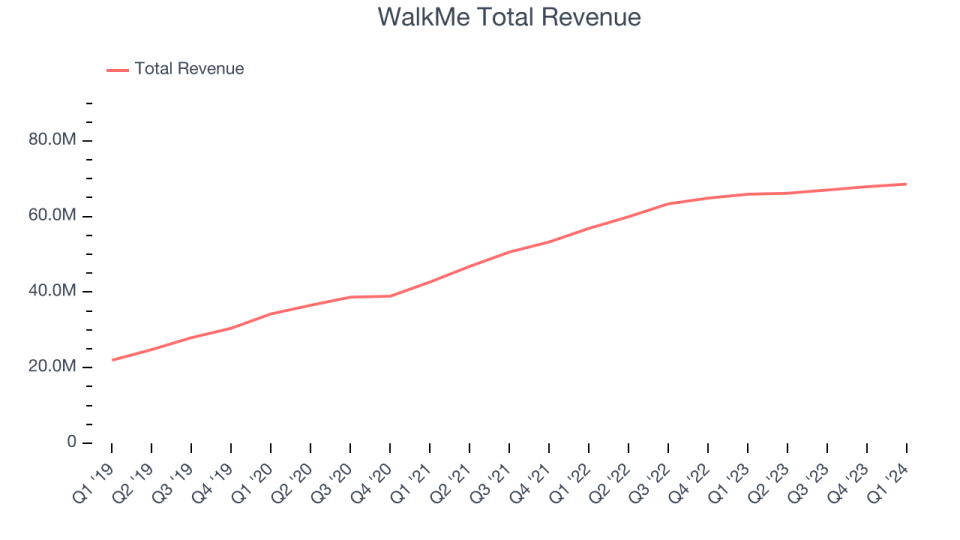

As you can see below, WalkMe's revenue growth has been solid over the last three years, growing from $42.65 million in Q1 2021 to $68.57 million this quarter.

WalkMe's quarterly revenue was only up 4.1% year on year, which might disappoint some shareholders. Additionally, its growth did slow down compared to last quarter as the company's revenue increased by just $685,000 in Q1 compared to $874,000 in Q4 CY2023. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Next quarter's guidance suggests that WalkMe is expecting revenue to grow 5.1% year on year to $69.5 million, slowing down from the 10.4% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 6.4% over the next 12 months before the earnings results announcement.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

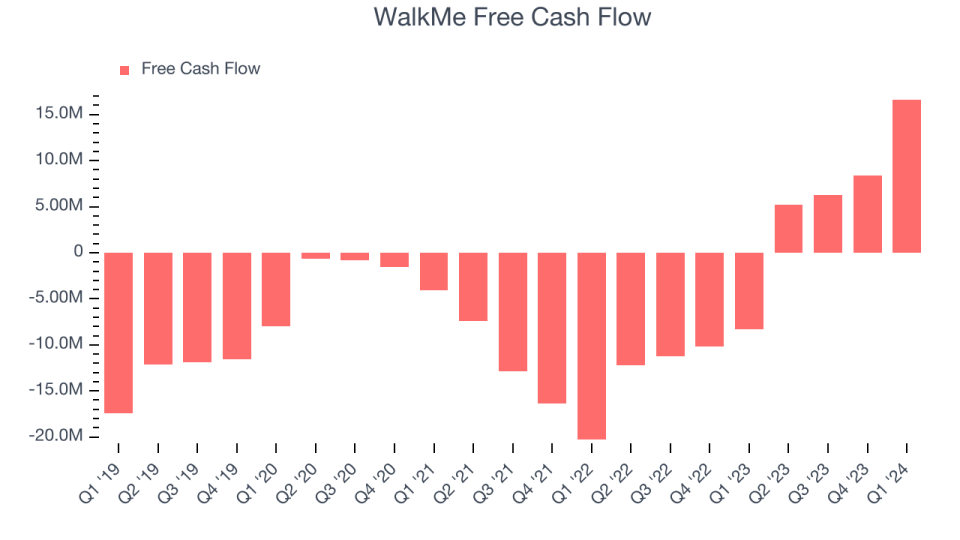

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. WalkMe's free cash flow came in at $16.64 million in Q1, turning positive over the last year.

WalkMe has generated $36.4 million in free cash flow over the last 12 months, a decent 13.5% of revenue. This FCF margin stems from its asset-lite business model and gives it a decent amount of cash to reinvest in its business.

Key Takeaways from WalkMe's Q1 Results

We enjoyed seeing WalkMe exceed analysts' billings expectations this quarter, which led to a small revenue beat. Operating profit and EPS beat by more convincing amounts. Additionally, while full year revenue guidance was maintained, full year operating profit guidance was raised, showing that the company is growing more efficiently. Overall, this quarter's results were solid and shareholders should feel optimistic. The stock is up 1.3% after reporting and currently trades at $7.93 per share.

So should you invest in WalkMe right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.