Yahoo Finance

Yahoo Finance Venturex Resources Limited's (ASX:VXR) Profit Outlook

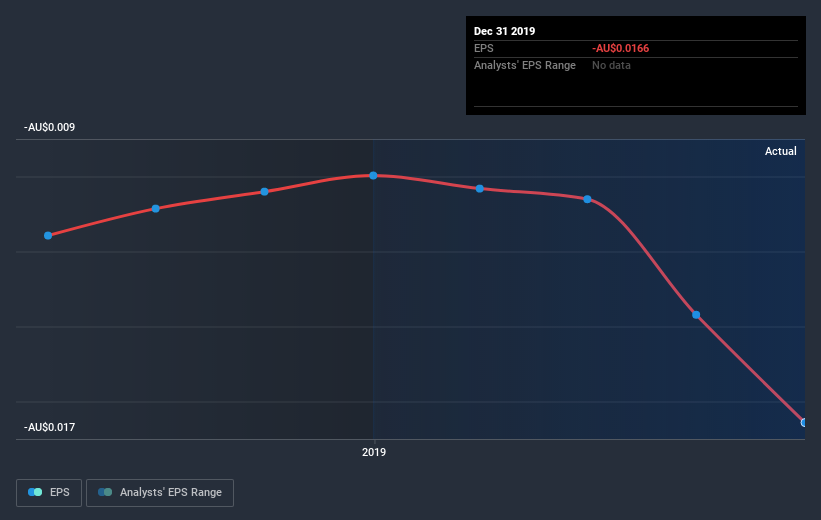

Venturex Resources Limited's (ASX:VXR): Venturex Resources Limited, together with its subsidiaries, engages in the exploration and development of mineral resources in Australia. The AU$23m market-cap posted a loss in its most recent financial year of AU$2.7m and a latest trailing-twelve-month loss of AU$4.5m leading to an even wider gap between loss and breakeven. The most pressing concern for investors is VXR’s path to profitability – when will it breakeven? In this article, I will touch on the expectations for VXR’s growth and when analysts expect the company to become profitable.

Check out our latest analysis for Venturex Resources

According to the industry analysts covering VXR, breakeven is near. They expect the company to post a final loss in 2021, before turning a profit of AU$2.3m in 2022. VXR is therefore projected to breakeven around 2 years from today. In order to meet this breakeven date, I calculated the rate at which VXR must grow year-on-year. It turns out an average annual growth rate of 73% is expected, which signals high confidence from analysts. If this rate turns out to be too aggressive, VXR may become profitable much later than analysts predict.

Underlying developments driving VXR’s growth isn’t the focus of this broad overview, but, keep in mind that typically a metal and mining business has lumpy cash flows which are contingent on the natural resource mined and stage at which the company is operating. This means that a high growth rate is not unusual, especially if the company is currently in an investment period.

One thing I’d like to point out is that VXR has managed its capital judiciously, with debt making up 8.5% of equity. This means that VXR has predominantly funded its operations from equity capital,and its low debt obligation reduces the risk around investing in the loss-making company.

Next Steps:

There are too many aspects of VXR to cover in one brief article, but the key fundamentals for the company can all be found in one place – VXR’s company page on Simply Wall St. I’ve also compiled a list of pertinent aspects you should further research:

Valuation: What is VXR worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether VXR is currently mispriced by the market.

Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Venturex Resources’s board and the CEO’s back ground.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.