Yahoo Finance

Yahoo Finance Some Tigers Realm Coal (ASX:TIG) Shareholders Have Taken A Painful 74% Share Price Drop

Some stocks are best avoided. We really hate to see fellow investors lose their hard-earned money. For example, we sympathize with anyone who was caught holding Tigers Realm Coal Limited (ASX:TIG) during the five years that saw its share price drop a whopping 74%.

See our latest analysis for Tigers Realm Coal

Tigers Realm Coal isn’t a profitable company, so it is unlikely we’ll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

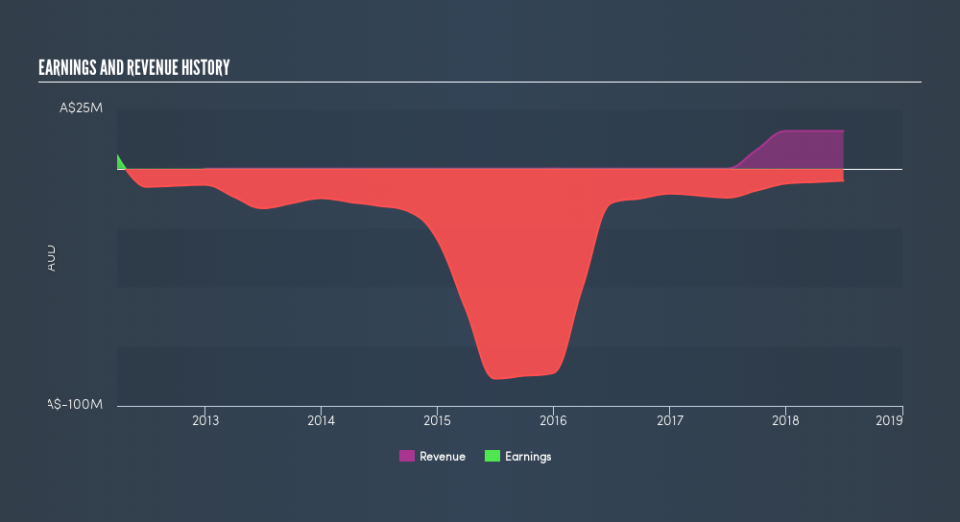

In the last half decade, Tigers Realm Coal saw its revenue increase by 93% per year. That’s well above most other pre-profit companies. So on the face of it we’re really surprised to see the share price has averaged a fall of 24% each year, in the same time period. It could be that the stock was over-hyped before. We’d recommend carefully checking for indications of future growth – and balance sheet threats – before considering a purchase.

Depicted in the graphic below, you’ll see revenue and earnings over time. If you want more detail, you can click on the chart itself.

This free interactive report on Tigers Realm Coal’s balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

Investors in Tigers Realm Coal had a tough year, with a total loss of 11%, against a market gain of about 8.0%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. However, the loss over the last year isn’t as bad as the 24% per annum loss investors have suffered over the last half decade. We’d need to see some sustained improvements in the key metrics before we could muster much enthusiasm. If you would like to research Tigers Realm Coal in more detail then you might want to take a look at whether insiders have been buying or selling shares in the company.

If you would prefer to check out another company — one with potentially superior financials — then do not miss this free list of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.