Yahoo Finance

Yahoo Finance Should You Be Tempted To Sell IRESS Limited (ASX:IRE) Because Of Its P/E Ratio?

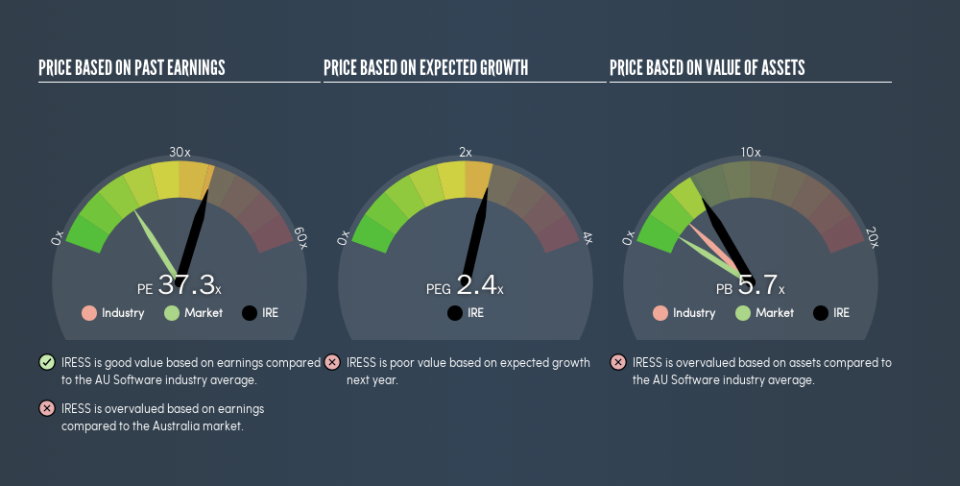

The goal of this article is to teach you how to use price to earnings ratios (P/E ratios). We'll look at IRESS Limited's (ASX:IRE) P/E ratio and reflect on what it tells us about the company's share price. IRESS has a price to earnings ratio of 37.29, based on the last twelve months. That means that at current prices, buyers pay A$37.29 for every A$1 in trailing yearly profits.

View our latest analysis for IRESS

How Do I Calculate A Price To Earnings Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Share Price ÷ Earnings per Share (EPS)

Or for IRESS:

P/E of 37.29 = A$14.02 ÷ A$0.38 (Based on the trailing twelve months to December 2018.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio implies that investors pay a higher price for the earning power of the business. That is not a good or a bad thing per se, but a high P/E does imply buyers are optimistic about the future.

How Does IRESS's P/E Ratio Compare To Its Peers?

We can get an indication of market expectations by looking at the P/E ratio. You can see in the image below that the average P/E (37.3) for companies in the software industry is roughly the same as IRESS's P/E.

Its P/E ratio suggests that IRESS shareholders think that in the future it will perform about the same as other companies in its industry classification. The company could surprise by performing better than average, in the future. Further research into factors such as insider buying and selling, could help you form your own view on whether that is likely.

How Growth Rates Impact P/E Ratios

Earnings growth rates have a big influence on P/E ratios. If earnings are growing quickly, then the 'E' in the equation will increase faster than it would otherwise. Therefore, even if you pay a high multiple of earnings now, that multiple will become lower in the future. And as that P/E ratio drops, the company will look cheap, unless its share price increases.

IRESS's earnings per share grew by -6.2% in the last twelve months. And its annual EPS growth rate over 5 years is 16%.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

It's important to note that the P/E ratio considers the market capitalization, not the enterprise value. Thus, the metric does not reflect cash or debt held by the company. Theoretically, a business can improve its earnings (and produce a lower P/E in the future) by investing in growth. That means taking on debt (or spending its cash).

Spending on growth might be good or bad a few years later, but the point is that the P/E ratio does not account for the option (or lack thereof).

Is Debt Impacting IRESS's P/E?

IRESS's net debt is 7.2% of its market cap. So it doesn't have as many options as it would with net cash, but its debt would not have much of an impact on its P/E ratio.

The Verdict On IRESS's P/E Ratio

IRESS trades on a P/E ratio of 37.3, which is above its market average of 16.3. With modest debt relative to its size, and modest earnings growth, the market is likely expecting sustained long-term growth, if not a near-term improvement.

When the market is wrong about a stock, it gives savvy investors an opportunity. As value investor Benjamin Graham famously said, 'In the short run, the market is a voting machine but in the long run, it is a weighing machine.' So this free report on the analyst consensus forecasts could help you make a master move on this stock.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with modest (or no) debt, trading on a P/E below 20.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.