Yahoo Finance

Yahoo Finance A Spotlight On Alumina Limited's (ASX:AWC) Fundamentals

Alumina Limited (ASX:AWC) is a company with exceptional fundamental characteristics. Upon building up an investment case for a stock, we should look at various aspects. In the case of AWC, it is a company with great financial health as well as a a great track record of performance. In the following section, I expand a bit more on these key aspects. If you're interested in understanding beyond my broad commentary, take a look at the report on Alumina here.

Excellent balance sheet with solid track record

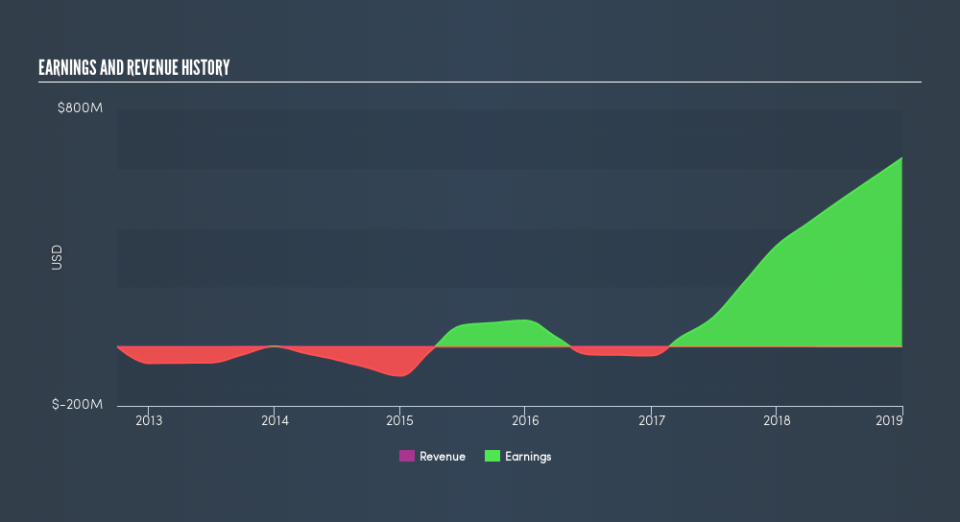

AWC delivered a bottom-line expansion of 87% in the prior year, with its most recent earnings level surpassing its average level over the last five years. This strong performance generated a robust double-digit return on equity of 30%, which is what investors like to see! AWC's strong financial health means that all of its upcoming liability payments are able to be met by its current cash and short-term investment holdings. This implies that AWC manages its cash and cost levels well, which is a crucial insight into the health of the company. AWC's has produced operating cash levels of 5.99x total debt over the past year, which implies that AWC's management has put its borrowings into good use by generating enough cash to cover a sufficient portion of borrowings.

Next Steps:

For Alumina, I've compiled three important aspects you should look at:

Future Outlook: What are well-informed industry analysts predicting for AWC’s future growth? Take a look at our free research report of analyst consensus for AWC’s outlook.

Valuation: What is AWC worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether AWC is currently mispriced by the market.

Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of AWC? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.