Yahoo Finance

Yahoo Finance Is Sims (ASX:SGM) A Risky Investment?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Sims Limited (ASX:SGM) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Sims

How Much Debt Does Sims Carry?

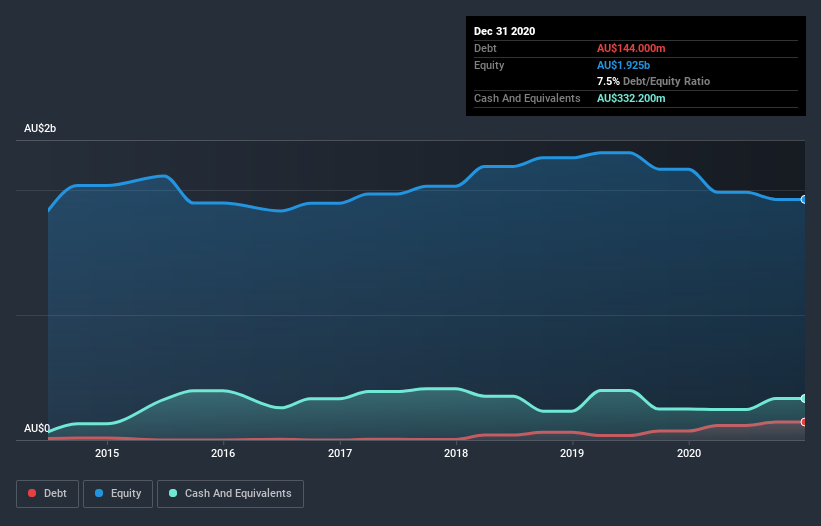

As you can see below, at the end of December 2020, Sims had AU$144.0m of debt, up from AU$71.7m a year ago. Click the image for more detail. But on the other hand it also has AU$332.2m in cash, leading to a AU$188.2m net cash position.

A Look At Sims' Liabilities

We can see from the most recent balance sheet that Sims had liabilities of AU$598.1m falling due within a year, and liabilities of AU$625.0m due beyond that. Offsetting these obligations, it had cash of AU$332.2m as well as receivables valued at AU$398.1m due within 12 months. So its liabilities total AU$492.8m more than the combination of its cash and short-term receivables.

Given Sims has a market capitalization of AU$3.03b, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, Sims also has more cash than debt, so we're pretty confident it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Sims can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Sims made a loss at the EBIT level, and saw its revenue drop to AU$4.7b, which is a fall of 23%. To be frank that doesn't bode well.

So How Risky Is Sims?

Statistically speaking companies that lose money are riskier than those that make money. And in the last year Sims had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of AU$6.1m and booked a AU$121m accounting loss. Given it only has net cash of AU$188.2m, the company may need to raise more capital if it doesn't reach break-even soon. Overall, we'd say the stock is a bit risky, and we're usually very cautious until we see positive free cash flow. When we look at a riskier company, we like to check how their profits (or losses) are trending over time. Today, we're providing readers this interactive graph showing how Sims's profit, revenue, and operating cashflow have changed over the last few years.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.