Yahoo Finance

Yahoo Finance Would Shareholders Who Purchased Titomic's (ASX:TTT) Stock Three Years Be Happy With The Share price Today?

Investing in stocks inevitably means buying into some companies that perform poorly. But the long term shareholders of Titomic Limited (ASX:TTT) have had an unfortunate run in the last three years. Regrettably, they have had to cope with a 54% drop in the share price over that period. And over the last year the share price fell 30%, so we doubt many shareholders are delighted. And the share price decline continued over the last week, dropping some 6.8%. However, this move may have been influenced by the broader market, which fell 2.8% in that time.

View our latest analysis for Titomic

Titomic wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. Shareholders of unprofitable companies usually expect strong revenue growth. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

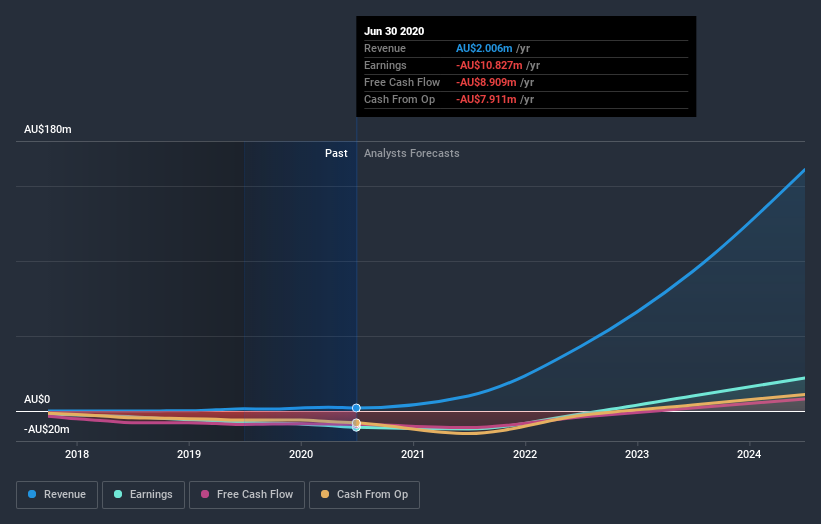

In the last three years, Titomic saw its revenue grow by 102% per year, compound. That's well above most other pre-profit companies. The share price has moved in quite the opposite direction, down 16% over that time, a bad result. It seems likely that the market is worried about the continual losses. But a share price drop of that magnitude could well signal that the market is overly negative on the stock.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

We like that insiders have been buying shares in the last twelve months. Having said that, most people consider earnings and revenue growth trends to be a more meaningful guide to the business. This free report showing analyst forecasts should help you form a view on Titomic

A Different Perspective

The last twelve months weren't great for Titomic shares, which cost holders 30%, while the market was up about 3.0%. Of course the long term matters more than the short term, and even great stocks will sometimes have a poor year. The three-year loss of 16% per year isn't as bad as the last twelve months, suggesting that the company has not been able to convince the market it has solved its problems. We would be wary of buying into a company with unsolved problems, although some investors will buy into struggling stocks if they believe the price is sufficiently attractive. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Case in point: We've spotted 3 warning signs for Titomic you should be aware of.

Titomic is not the only stock that insiders are buying. For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.