Yahoo Finance

Yahoo Finance Reasons Why You Should Retain ResMed (RMD) Stock For Now

ResMed Inc. RMD is gaining from continued demand for its sleep and respiratory care devices. The company posted better-than-expected results for the second quarter of fiscal 2023. Increased demand for the company’s digital health solution is impressive. However, mounting operating costs and stiff competition raise apprehensions.

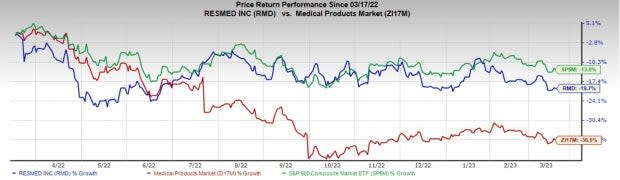

In the past year, the Zacks Rank #3 (Hold) stock has lost 19.7% compared with a 36.5% fall of the industry and a 13% decline of the S&P 500.

The renowned medical device company has a market capitalization of $30.56 billion. Its earnings for the second quarter of fiscal 2023 surpassed the Zacks Consensus Estimate by 3.8%. The company has a long-term expected growth rate of 16.6% compared with the industry’s 14.6% rise.

Let’s delve deeper.

Factors At Play

Q2 Upsides: ResMed exited the second quarter of fiscal 2023 with better-than-expected earnings and revenues. The company recorded a robust sales performance in the quarter on increased demand for sleep and respiratory care devices. Mask sales growth was strong across the globe, reflecting a post-COVID pandemic awareness about the importance and need for respiratory hygiene and respiratory health. The company registered strong customer uptake of the re-engineered AirSense 10 Card-to-Cloud device.

COVID-19-Led Critical Care Drives Demand for Products: ResMed’s business received a significant boost amid the pandemic on the back of strong demand for critical care products like ventilators and masks.

During the fiscal second-quarter update, the company continues to drive growth, banking on the strong adoption of ventilator devices around the world. The company witnessed good uptake of the life support and non-life support ventilator platforms during the quarter. There is also ongoing adoption of Propeller's monitoring system.

Potential in Digital Health: Of late, ResMed has been focusing on digital health technology. Amid the pandemic, ResMed saw increased global demand for its digital health solutions with the robust adoption of remote patient engagement and population health management.

Image Source: Zacks Investment Research

During its earnings call for the fiscal second quarter, ResMed noted that it has over 12.5 billion medical data in the cloud and over 18.5 million cloud-connectable medical devices on bedside tables in 140 countries worldwide. ResMed’s aims to improve 250 million lives through better health care in 2025.

Downsides

Mounting Costs: During the quarter, ResMed’s selling, general and administrative expenses rose 14.2% year over year, predominantly on increases in employee-related expenses, professional service fees and travel expenses. Meanwhile, research and development expenses increased 11.8%. These mounting expenses led to an adjusted operating margin contraction of 36 bps year over year to 29.6%, denting the company’s bottom line.

Competitive Landscape: The market for SDB products is highly competitive with respect to product price, features and reliability. ResMed's primary competitors include Philips BV; DeVilbiss Healthcare; Fisher & Paykel Healthcare Corporation Limited; Apex Medical Corporation; BMC Medical Co. Ltd.; and regional manufacturers.

Estimate Trend

Over the past 30 days, the Zacks Consensus Estimate for ResMed’s fiscal 2023 earnings has been constant at $6.38.

The Zacks Consensus Estimate for its fiscal 2023 revenues is pegged at $4.08 billion, suggesting a 14% rise from the 2022 comparable figure.

Key Picks

Few top-ranked stocks in the overall healthcare sector include Haemonetics Corporation HAE, TerrAscend Corp. TRSSF and Akerna Corp. KERN. Haemonetics and TerrAscend both sport a Zacks Rank #1, while Akerna carries a Zack Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Haemonetics’ stock has surged 42.1% in the past year. Earnings Estimates for Haemonetics have increased from $2.87 per share to 2.91 for 2023 and from $3.02 per share to $3.28 for 2024 in the past 30 days.

HAE’s earnings beat estimates in each of the last four quarters, delivering an average surprise of 10.98%. In the last reported quarter, it reported an earnings surprise of 7.59%.

Estimates for TerrAscend in 2023 have remained constant at a loss of 10 cents per share in the past 30 days. Shares of TerrAscend have declined 70.6% in the past year.

TerrAscend’s earnings beat estimates in one of the last three quarters and missed the mark in the other two, the average negative surprise being 136.11%. In the last reported quarter, TRSSF delivered an earnings surprise of 216.67%.

Akerna’s stock declined 95.7% in the past year. Its estimates for 2023 have remained constant at a loss of $1.91 per share over the past 30 days.

Akerna missed earnings estimates in each of the last four quarters, delivering a negative earnings surprise of 15.49%, on average. In the last reported quarter, KERN delivered a negative earnings surprise of 13.33%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ResMed Inc. (RMD) : Free Stock Analysis Report

Haemonetics Corporation (HAE) : Free Stock Analysis Report

Akerna Corp. (KERN) : Free Stock Analysis Report

TerrAscend Corp. (TRSSF) : Free Stock Analysis Report