Yahoo Finance

Yahoo Finance Is Papyrus Australia's (ASX:PPY) Share Price Gain Of 140% Well Earned?

The last three months have been tough on Papyrus Australia Limited (ASX:PPY) shareholders, who have seen the share price decline a rather worrying 40%. But that doesn't change the fact that the returns over the last year have been very strong. Like an eagle, the share price soared 140% in that time. So it is important to view the recent reduction in price through that lense. Investors should be wondering whether the business itself has the fundamental value required to continue to drive gains.

See our latest analysis for Papyrus Australia

We don't think Papyrus Australia's revenue of AU$4,599 is enough to establish significant demand. So it seems shareholders are too busy dreaming about the progress to come than dwelling on the current (lack of) revenue. Investors will be hoping that Papyrus Australia can make progress and gain better traction for the business, before it runs low on cash.

As a general rule, if a company doesn't have much revenue, and it loses money, then it is a high risk investment. There was already a significant chance that they would need more money for business development, and indeed they recently put themselves at the mercy of capital markets and raised equity. So the share price itself impacts the value of the shares (as it determines the cost of capital). While some such companies do very well over the long term, others become hyped up by promoters before eventually falling back down to earth, and going bankrupt (or being recapitalized). Some Papyrus Australia investors have already had a taste of the sweet taste stocks like this can leave in the mouth, as they gain popularity and attract speculative capital.

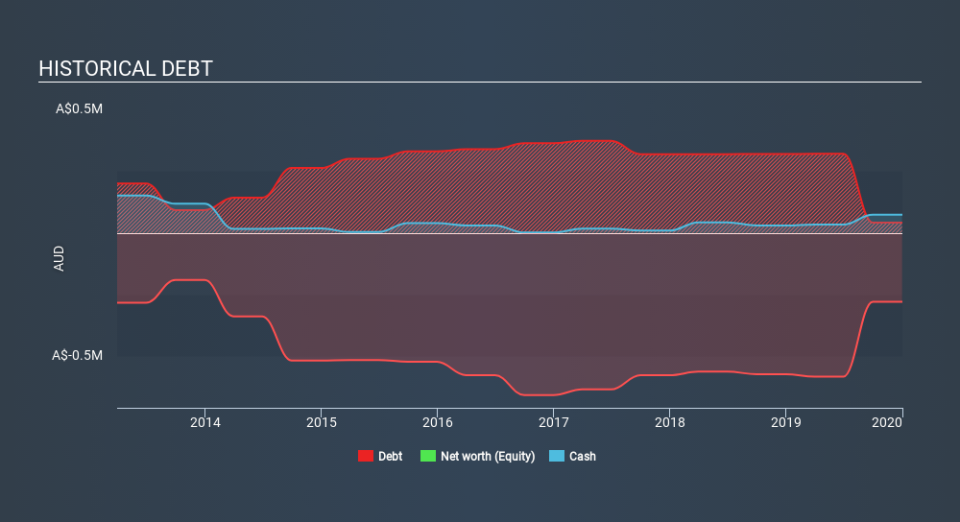

Our data indicates that Papyrus Australia had more in total liabilities than it had cash, when it last reported. That made it extremely high risk, in our view. So we're not surprised to see the stock up 87% in the last year , once the company took on some more capital. It's clear more than a few people believe in the potential. The image below shows how Papyrus Australia's balance sheet has changed over time; if you want to see the precise values, simply click on the image.

It can be extremely risky to invest in a company that doesn't even have revenue. There's no way to know its value easily. One thing you can do is check if company insiders are buying shares. If they are buying a significant amount of shares, that's certainly a good thing. Luckily we are in a position to provide you with this free chart of insider buying (and selling).

A Different Perspective

We're pleased to report that Papyrus Australia shareholders have received a total shareholder return of 140% over one year. There's no doubt those recent returns are much better than the TSR loss of 1.6% per year over five years. The long term loss makes us cautious, but the short term TSR gain certainly hints at a brighter future. It's always interesting to track share price performance over the longer term. But to understand Papyrus Australia better, we need to consider many other factors. Take risks, for example - Papyrus Australia has 5 warning signs (and 3 which are a bit unpleasant) we think you should know about.

Of course Papyrus Australia may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.