Yahoo Finance

Yahoo Finance How Much Is Edison International (NYSE:EIX) Paying Its CEO?

Pedro Pizarro became the CEO of Edison International (NYSE:EIX) in 2016, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also look to assess whether the CEO is appropriately paid, considering recent earnings growth and investor returns for Edison International.

Check out our latest analysis for Edison International

How Does Total Compensation For Pedro Pizarro Compare With Other Companies In The Industry?

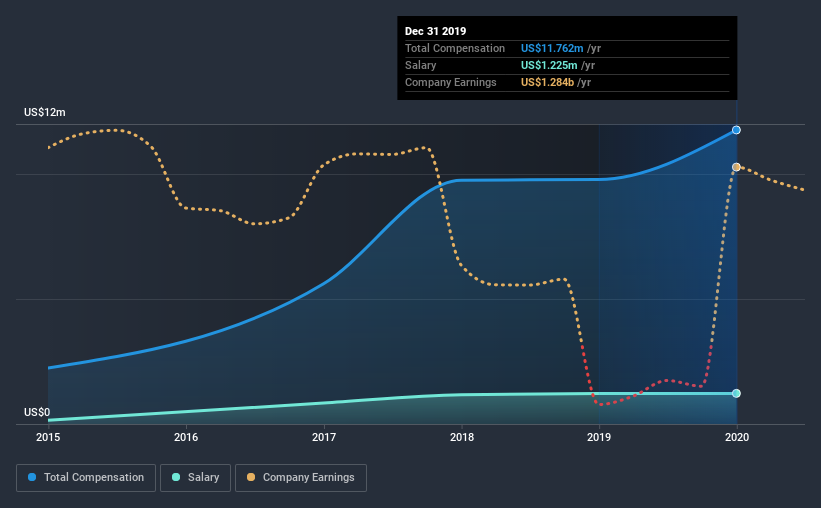

At the time of writing, our data shows that Edison International has a market capitalization of US$20b, and reported total annual CEO compensation of US$12m for the year to December 2019. Notably, that's an increase of 20% over the year before. We think total compensation is more important but our data shows that the CEO salary is lower, at US$1.2m.

In comparison with other companies in the industry with market capitalizations over US$8.0b , the reported median total CEO compensation was US$14m. So it looks like Edison International compensates Pedro Pizarro in line with the median for the industry. Furthermore, Pedro Pizarro directly owns US$3.3m worth of shares in the company.

Component | 2019 | 2018 | Proportion (2019) |

Salary | US$1.2m | US$1.2m | 10% |

Other | US$11m | US$8.6m | 90% |

Total Compensation | US$12m | US$9.8m | 100% |

Speaking on an industry level, nearly 14% of total compensation represents salary, while the remainder of 86% is other remuneration. Edison International pays a modest slice of remuneration through salary, as compared to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

Edison International's Growth

Edison International has reduced its earnings per share by 9.9% a year over the last three years. It saw its revenue drop 3.3% over the last year.

The decline in EPS is a bit concerning. And the impression is worse when you consider revenue is down year-on-year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Edison International Been A Good Investment?

Since shareholders would have lost about 26% over three years, some Edison International investors would surely be feeling negative emotions. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

In Summary...

As we noted earlier, Edison International pays its CEO in line with similar-sized companies belonging to the same industry. In the meantime, the company has reported declining EPS growth and shareholder returns over the last three years. It's tough to call out the compensation as inappropriate, but shareholders might not favor a raise before company performance improves.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. That's why we did our research, and identified 3 warning signs for Edison International (of which 1 makes us a bit uncomfortable!) that you should know about in order to have a holistic understanding of the stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.