Yahoo Finance

Yahoo Finance How Much Did Heritage Financial Corporation’s (NASDAQ:HFWA) CEO Pocket Last Year?

Leading Heritage Financial Corporation (NASDAQ:HFWA) as the CEO, Brian Vance took the company to a valuation of US$1.31b. Understanding how CEOs are incentivised to run and grow their company is an important aspect of investing in a stock. Incentives can be in the form of compensation, which should always be structured in a way that promotes value-creation to shareholders. Today we will assess Vance’s pay and compare this to the company’s performance over the same period, as well as measure it against other US CEOs leading companies of similar size and profitability.

View our latest analysis for Heritage Financial

What has HFWA’s performance been like?

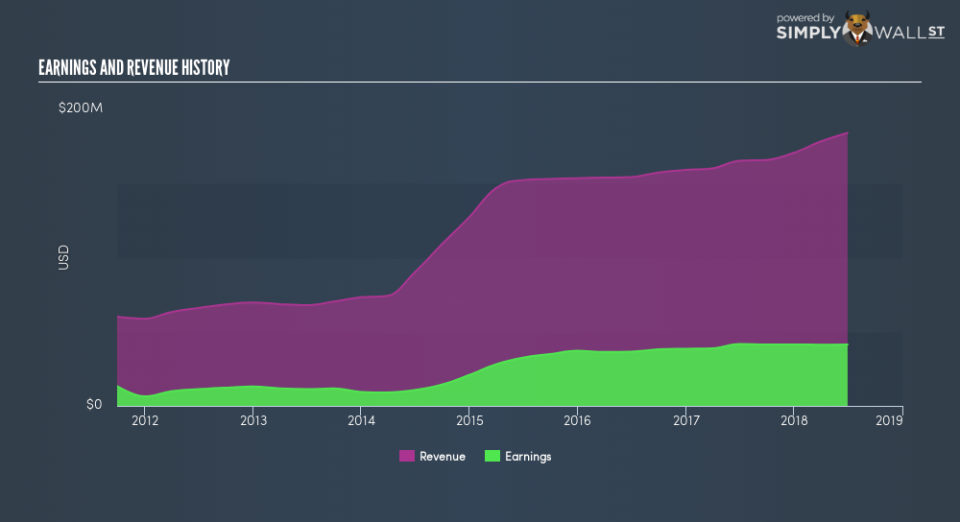

Earnings is a powerful indication of HFWA’s ability to invest shareholders’ funds and generate returns. Therefore I will use earnings as a proxy of Vance’s performance in the past year. Over the last year HFWA produced a profit of US$41.35m compared to its prior year’s earnings of US$41.73m – a decline of -0.91%. However, HFWA has strived to maintain a good track record of profitability, given its average EPS of US$0.99 over the past couple of years. In the situation of falling profits, the company may be going through a period of reinvestment and growth, or it can be an indication of some headwind. Regardless, CEO compensation should echo the current condition of the business. In the latest financial statments, Vance’s total remuneration grew by 20.16% to US$1.31m. Moreover, Vance’s pay is also made up of 20.46% non-cash elements, which means that fluctuations in HFWA’s share price can impact the actual level of what the CEO actually receives.

Is HFWA overpaying the CEO?

Even though one size does not fit all, since remuneration should account for specific factors of the company and market, we can determine a high-level base line to see if HFWA is an outlier. This outcome can help shareholders ask the right question about Vance’s incentive alignment. Typically, a US small-cap has a value of $1B, generates earnings of $96M, and pays its CEO circa $2.7M per year. Based on HFWA’s size and performance, in terms of market cap and earnings, it seems that Vance is paid lower than other similar US CEOs in the small-cap industry.

Next Steps:

In order to determine whether or not you should invest in HFWA, your thesis should be built on fundamentals. Even though CEO pay isn’t technically a key concern, it could serve as an indication as to how board members align incentives and how they think about setting policies. These issues directly impacts how HFWA makes money, and factors impacting your return on investment. If you have not done so already, I urge you to complete your research by taking a look at the following:

Governance: To find out more about HFWA’s governance, look through our infographic report of the company’s board and management.

Financial Health: Does it have a healthy balance sheet? Take a look at our free balance sheet analysis with six simple checks on key factors like leverage and risk.

Other High-Growth Alternatives: Are there other high-growth stocks you could be holding instead of HFWA? Explore our interactive list of stocks with large growth potential to get an idea of what else is out there you may be missing!

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.