Yahoo Finance

Yahoo Finance Is MGM China Holdings (HKG:2282) Using Too Much Debt?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that MGM China Holdings Limited (HKG:2282) does use debt in its business. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for MGM China Holdings

What Is MGM China Holdings's Debt?

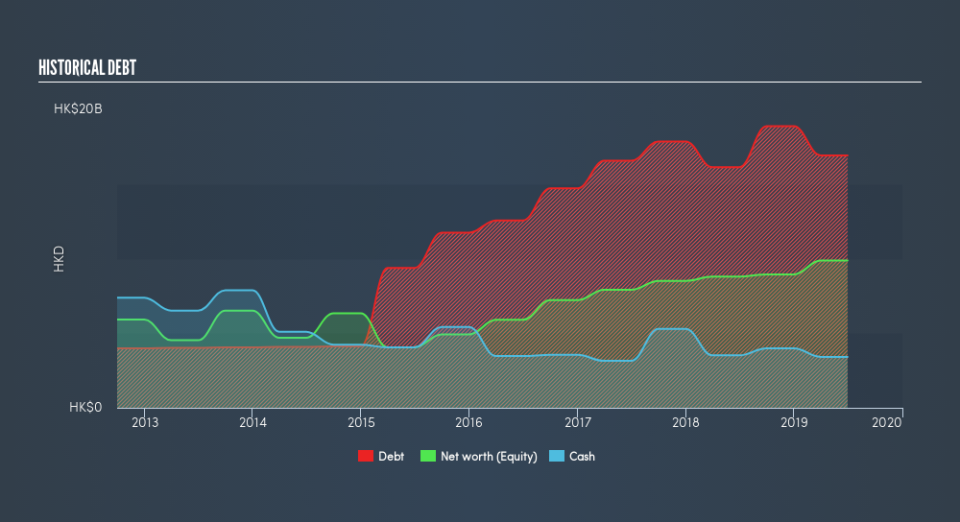

You can click the graphic below for the historical numbers, but it shows that as of June 2019 MGM China Holdings had HK$16.9b of debt, an increase on HK$16.1b, over one year. However, it also had HK$3.42b in cash, and so its net debt is HK$13.5b.

How Strong Is MGM China Holdings's Balance Sheet?

We can see from the most recent balance sheet that MGM China Holdings had liabilities of HK$7.03b falling due within a year, and liabilities of HK$17.1b due beyond that. Offsetting these obligations, it had cash of HK$3.42b as well as receivables valued at HK$358.2m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by HK$20.4b.

While this might seem like a lot, it is not so bad since MGM China Holdings has a market capitalization of HK$42.9b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

MGM China Holdings's debt is 2.8 times its EBITDA, and its EBIT cover its interest expense 3.0 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. On a lighter note, we note that MGM China Holdings grew its EBIT by 27% in the last year. If it can maintain that kind of improvement, its debt load will begin to melt away like glaciers in a warming world. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if MGM China Holdings can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, MGM China Holdings reported free cash flow worth 5.2% of its EBIT, which is really quite low. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

Neither MGM China Holdings's ability to convert EBIT to free cash flow nor its interest cover gave us confidence in its ability to take on more debt. But the good news is it seems to be able to grow its EBIT with ease. Looking at all the angles mentioned above, it does seem to us that MGM China Holdings is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of MGM China Holdings's earnings per share history for free.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.