Yahoo Finance

Yahoo Finance Is MAXIMUS (NYSE:MMS) A Risky Investment?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies MAXIMUS, Inc. (NYSE:MMS) makes use of debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for MAXIMUS

How Much Debt Does MAXIMUS Carry?

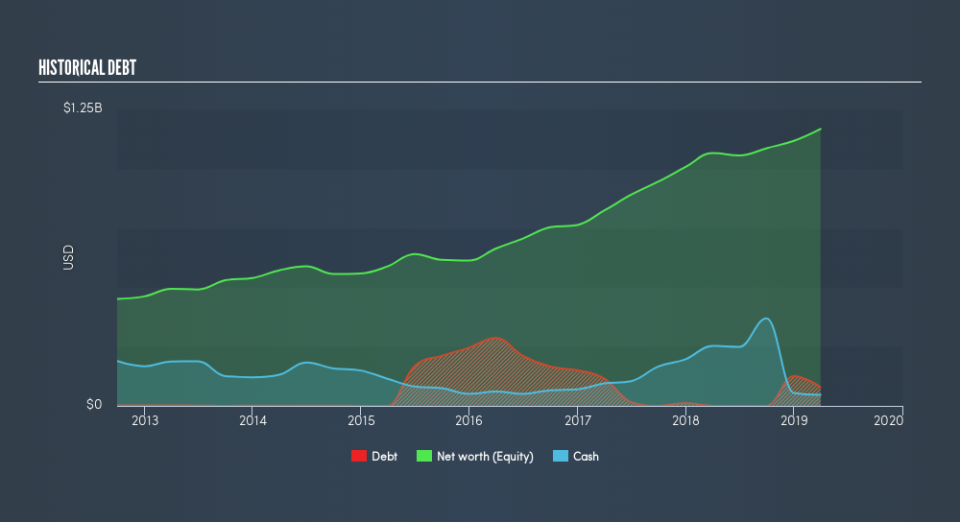

You can click the graphic below for the historical numbers, but it shows that as of March 2019 MAXIMUS had US$79.0m of debt, an increase on none, over one year. However, it does have US$46.8m in cash offsetting this, leading to net debt of about US$32.2m.

How Healthy Is MAXIMUS's Balance Sheet?

We can see from the most recent balance sheet that MAXIMUS had liabilities of US$320.8m falling due within a year, and liabilities of US$199.4m due beyond that. Offsetting these obligations, it had cash of US$46.8m as well as receivables valued at US$643.5m due within 12 months. So it actually has US$170.2m more liquid assets than total liabilities.

This surplus suggests that MAXIMUS has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Carrying virtually no net debt, MAXIMUS has a very light debt load indeed.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

MAXIMUS has barely any net debt, as demonstrated by its net debt to EBITDA ratio of only 0.089. Humorously, it actually received more in interest over the last twelve months than it had to pay. So there's no doubt this company can take on debt as easily as enthusiastic spray-tanners take on an orange hue. On the other hand, MAXIMUS saw its EBIT drop by 2.3% in the last twelve months. That sort of decline, if sustained, will obviously make debt harder to handle. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if MAXIMUS can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. During the last three years, MAXIMUS generated free cash flow amounting to a very robust 91% of its EBIT, more than we'd expect. That positions it well to pay down debt if desirable to do so.

Our View

Happily, MAXIMUS's impressive interest cover implies it has the upper hand on its debt. But, on a more sombre note, we are a little concerned by its EBIT growth rate. Zooming out, MAXIMUS seems to use debt quite reasonably; and that gets the nod from us. While debt does bring risk, when used wisely it can also bring a higher return on equity. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that MAXIMUS insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.