Yahoo Finance

Yahoo Finance Is Magontec Limited (ASX:MGL) Excessively Paying Its CEO?

The CEO of Magontec Limited (ASX:MGL) is Nick Andrews. First, this article will compare CEO compensation with compensation at similar sized companies. Next, we'll consider growth that the business demonstrates. Third, we'll reflect on the total return to shareholders over three years, as a second measure of business performance. This method should give us information to assess how appropriately the company pays the CEO.

Check out our latest analysis for Magontec

How Does Nick Andrews's Compensation Compare With Similar Sized Companies?

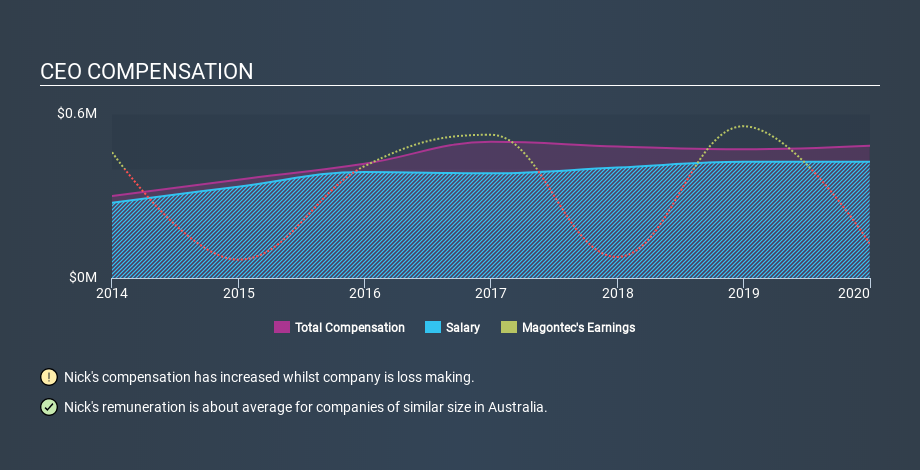

Our data indicates that Magontec Limited is worth AU$18m, and total annual CEO compensation was reported as AU$484k for the year to December 2019. That's a fairly small increase of 2.8% on year before. We think total compensation is more important but we note that the CEO salary is lower, at AU$425k. We examined a group of similar sized companies, with market capitalizations of below AU$312m. The median CEO total compensation in that group is AU$392k.

Pay mix tells us a lot about how a company functions versus the wider industry, and it's no different in the case of Magontec. Speaking on an industry level, we can see that nearly 69% of total compensation represents salary, while the remainder of 31% is other remuneration. Magontec is largely mirroring the industry average when it comes to the share a salary enjoys in overall compensation

So Nick Andrews is paid around the average of the companies we looked at. While this data point isn't particularly informative alone, it gains more meaning when considered with business performance. The graphic below shows how CEO compensation at Magontec has changed from year to year.

Is Magontec Limited Growing?

Magontec Limited has reduced its earnings per share by an average of 5.2% a year, over the last three years (measured with a line of best fit). The trailing twelve months of revenue was pretty much the same as the prior period.

Few shareholders would be pleased to read that earnings per share are lower over three years. And the flat revenue is seriously uninspiring. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Magontec Limited Been A Good Investment?

Since shareholders would have lost about 57% over three years, some Magontec Limited shareholders would surely be feeling negative emotions. So shareholders would probably think the company shouldn't be too generous with CEO compensation.

In Summary...

Nick Andrews is paid around what is normal for the leaders of comparable size companies.

The company isn't growing EPS, and shareholder returns have been disappointing. Most would consider it prudent for the company to hold off any CEO pay rise until performance improves. Taking a breather from CEO compensation, we've spotted 4 warning signs for Magontec (of which 1 is significant!) you should know about in order to have a holistic understanding of the stock.

Important note: Magontec may not be the best stock to buy. You might find something better in this list of interesting companies with high ROE and low debt.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.