Yahoo Finance

Yahoo Finance It Looks Like Dundee Corporation's (TSE:DC.A) CEO May Expect Their Salary To Be Put Under The Microscope

Key Insights

Dundee's Annual General Meeting to take place on 12th of June

Salary of CA$500.0k is part of CEO Jonathan Goodman's total remuneration

The total compensation is 540% higher than the average for the industry

Dundee's EPS declined by 7.2% over the past three years while total shareholder loss over the past three years was 10%

The results at Dundee Corporation (TSE:DC.A) have been quite disappointing recently and CEO Jonathan Goodman bears some responsibility for this. At the upcoming AGM on 12th of June, shareholders can hear from the board including their plans for turning around performance. They will also get a chance to influence managerial decision-making through voting on resolutions such as executive remuneration, which may impact firm value in the future. The data we present below explains why we think CEO compensation is not consistent with recent performance.

Check out our latest analysis for Dundee

How Does Total Compensation For Jonathan Goodman Compare With Other Companies In The Industry?

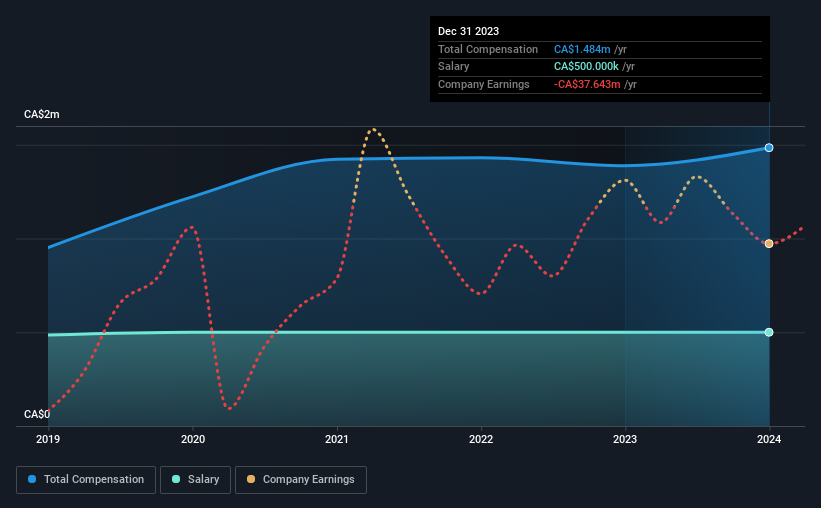

Our data indicates that Dundee Corporation has a market capitalization of CA$120m, and total annual CEO compensation was reported as CA$1.5m for the year to December 2023. That's just a smallish increase of 6.9% on last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at CA$500k.

In comparison with other companies in the Canadian Real Estate industry with market capitalizations under CA$274m, the reported median total CEO compensation was CA$232k. Hence, we can conclude that Jonathan Goodman is remunerated higher than the industry median. Moreover, Jonathan Goodman also holds CA$7.4m worth of Dundee stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

Component | 2023 | 2022 | Proportion (2023) |

Salary | CA$500k | CA$500k | 34% |

Other | CA$984k | CA$888k | 66% |

Total Compensation | CA$1.5m | CA$1.4m | 100% |

On an industry level, around 58% of total compensation represents salary and 42% is other remuneration. Dundee pays a modest slice of remuneration through salary, as compared to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Dundee Corporation's Growth

Dundee Corporation has reduced its earnings per share by 7.2% a year over the last three years. Its revenue is down 7.3% over the previous year.

Overall this is not a very positive result for shareholders. This is compounded by the fact revenue is actually down on last year. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Dundee Corporation Been A Good Investment?

Since shareholders would have lost about 10% over three years, some Dundee Corporation investors would surely be feeling negative emotions. So shareholders would probably want the company to be less generous with CEO compensation.

In Summary...

Not only have shareholders not seen a favorable return on their investment, but the business hasn't performed well either. Few shareholders would be willing to award the CEO with a pay raise. At the upcoming AGM, management will get a chance to explain how they plan to get the business back on track and address the concerns from investors.

CEO compensation can have a massive impact on performance, but it's just one element. We did our research and spotted 2 warning signs for Dundee that investors should look into moving forward.

Switching gears from Dundee, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.