Yahoo Finance

Yahoo Finance We Take A Look At Whether Curtiss-Wright Corporation's (NYSE:CW) CEO May Be Underpaid

Key Insights

Curtiss-Wright's Annual General Meeting to take place on 2nd of May

CEO Lynn Bamford's total compensation includes salary of US$989.2k

The overall pay is 43% below the industry average

Curtiss-Wright's EPS grew by 24% over the past three years while total shareholder return over the past three years was 98%

The impressive results at Curtiss-Wright Corporation (NYSE:CW) recently will be great news for shareholders. At the upcoming AGM on 2nd of May, they would be interested to hear about the company strategy going forward and get a chance to cast their votes on resolutions such as executive remuneration and other company matters. Here we will show why we think CEO compensation is appropriate and discuss the case for a pay rise.

View our latest analysis for Curtiss-Wright

Comparing Curtiss-Wright Corporation's CEO Compensation With The Industry

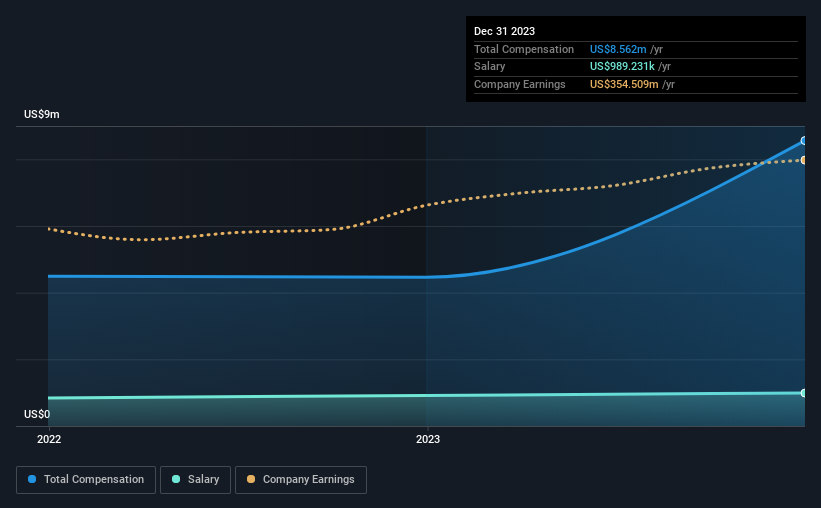

According to our data, Curtiss-Wright Corporation has a market capitalization of US$9.7b, and paid its CEO total annual compensation worth US$8.6m over the year to December 2023. That's a notable increase of 92% on last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$989k.

On comparing similar companies in the American Aerospace & Defense industry with market capitalizations above US$8.0b, we found that the median total CEO compensation was US$15m. In other words, Curtiss-Wright pays its CEO lower than the industry median. Moreover, Lynn Bamford also holds US$9.1m worth of Curtiss-Wright stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

Component | 2023 | 2022 | Proportion (2023) |

Salary | US$989k | US$918k | 12% |

Other | US$7.6m | US$3.5m | 88% |

Total Compensation | US$8.6m | US$4.5m | 100% |

On an industry level, around 23% of total compensation represents salary and 77% is other remuneration. Curtiss-Wright sets aside a smaller share of compensation for salary, in comparison to the overall industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at Curtiss-Wright Corporation's Growth Numbers

Curtiss-Wright Corporation has seen its earnings per share (EPS) increase by 24% a year over the past three years. Its revenue is up 11% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's also good to see decent revenue growth in the last year, suggesting the business is healthy and growing. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Curtiss-Wright Corporation Been A Good Investment?

We think that the total shareholder return of 98%, over three years, would leave most Curtiss-Wright Corporation shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

Given the company's decent performance, the CEO remuneration policy might not be shareholders' central point of focus in the AGM. In fact, strategic decisions that could impact the future of the business might be a far more interesting topic for investors as it would help them set their longer-term expectations.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 1 warning sign for Curtiss-Wright that you should be aware of before investing.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.