Yahoo Finance

Yahoo Finance Investors in Solaris Oilfield Infrastructure (NYSE:SOI) have unfortunately lost 50% over the last three years

For many investors, the main point of stock picking is to generate higher returns than the overall market. But in any portfolio, there are likely to be some stocks that fall short of that benchmark. Unfortunately, that's been the case for longer term Solaris Oilfield Infrastructure, Inc. (NYSE:SOI) shareholders, since the share price is down 55% in the last three years, falling well short of the market return of around 65%. The falls have accelerated recently, with the share price down 29% in the last three months.

With that in mind, it's worth seeing if the company's underlying fundamentals have been the driver of long term performance, or if there are some discrepancies.

Check out our latest analysis for Solaris Oilfield Infrastructure

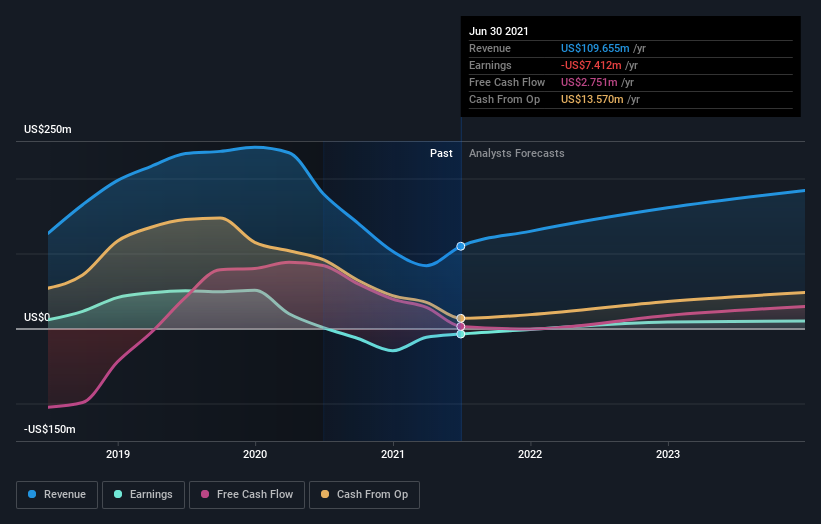

Solaris Oilfield Infrastructure isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. When a company doesn't make profits, we'd generally expect to see good revenue growth. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

Over the last three years, Solaris Oilfield Infrastructure's revenue dropped 15% per year. That's definitely a weaker result than most pre-profit companies report. With no profits and falling revenue it is no surprise that investors have been dumping the stock, pushing the price down by 16% per year over that time. When revenue is dropping, and losses are still costing, and the share price sinking fast, it's fair to ask if something is remiss. It could be a while before the company repays long suffering shareholders with share price gains.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

Balance sheet strength is crucial. It might be well worthwhile taking a look at our free report on how its financial position has changed over time.

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). Whereas the share price return only reflects the change in the share price, the TSR includes the value of dividends (assuming they were reinvested) and the benefit of any discounted capital raising or spin-off. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. As it happens, Solaris Oilfield Infrastructure's TSR for the last 3 years was -50%, which exceeds the share price return mentioned earlier. This is largely a result of its dividend payments!

A Different Perspective

Solaris Oilfield Infrastructure shareholders are up 5.3% for the year (even including dividends). While you don't go broke making a profit, this return was actually lower than the average market return of about 39%. The silver lining is that the recent rise is far preferable to the annual loss of 14% that shareholders have suffered over the last three years. It could well be that the business is stabilizing. It's always interesting to track share price performance over the longer term. But to understand Solaris Oilfield Infrastructure better, we need to consider many other factors. Consider risks, for instance. Every company has them, and we've spotted 2 warning signs for Solaris Oilfield Infrastructure you should know about.

Of course Solaris Oilfield Infrastructure may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.