Yahoo Finance

Yahoo Finance Investors in Matrix Composites & Engineering (ASX:MCE) have seen solid returns of 172% over the past three years

The most you can lose on any stock (assuming you don't use leverage) is 100% of your money. But in contrast you can make much more than 100% if the company does well. For example, the Matrix Composites & Engineering Ltd (ASX:MCE) share price has soared 162% in the last three years. Most would be happy with that. On top of that, the share price is up 25% in about a quarter.

So let's investigate and see if the longer term performance of the company has been in line with the underlying business' progress.

View our latest analysis for Matrix Composites & Engineering

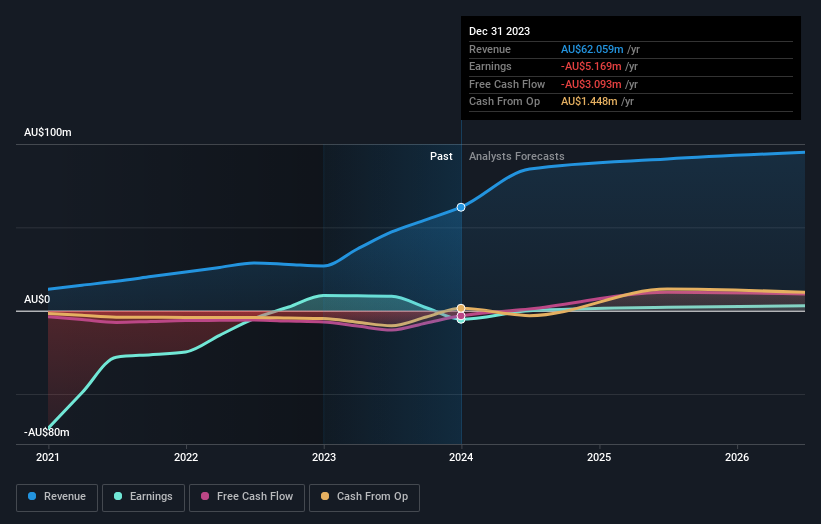

Because Matrix Composites & Engineering made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. Some companies are willing to postpone profitability to grow revenue faster, but in that case one would hope for good top-line growth to make up for the lack of earnings.

In the last 3 years Matrix Composites & Engineering saw its revenue grow at 48% per year. That's much better than most loss-making companies. Meanwhile, the share price performance has been pretty solid at 38% compound over three years. But it does seem like the market is paying attention to strong revenue growth. Nonetheless, we'd say Matrix Composites & Engineering is still worth investigating - successful businesses can often keep growing for long periods.

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

You can see how its balance sheet has strengthened (or weakened) over time in this free interactive graphic.

What About The Total Shareholder Return (TSR)?

We'd be remiss not to mention the difference between Matrix Composites & Engineering's total shareholder return (TSR) and its share price return. The TSR attempts to capture the value of dividends (as if they were reinvested) as well as any spin-offs or discounted capital raisings offered to shareholders. Dividends have been really beneficial for Matrix Composites & Engineering shareholders, and that cash payout contributed to why its TSR of 172%, over the last 3 years, is better than the share price return.

A Different Perspective

It's good to see that Matrix Composites & Engineering has rewarded shareholders with a total shareholder return of 21% in the last twelve months. That's better than the annualised return of 1.5% over half a decade, implying that the company is doing better recently. In the best case scenario, this may hint at some real business momentum, implying that now could be a great time to delve deeper. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider for instance, the ever-present spectre of investment risk. We've identified 1 warning sign with Matrix Composites & Engineering , and understanding them should be part of your investment process.

For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Australian exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.