Yahoo Finance

Yahoo Finance Imagine Owning Medlab Clinical (ASX:MDC) And Trying To Stomach The 75% Share Price Drop

Medlab Clinical Limited (ASX:MDC) shareholders should be happy to see the share price up 13% in the last month. But that doesn't change the fact that the returns over the last three years have been stomach churning. In that time the share price has melted like a snowball in the desert, down 75%. So it's about time shareholders saw some gains. But the more important question is whether the underlying business can justify a higher price still.

Check out our latest analysis for Medlab Clinical

Because Medlab Clinical made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. Shareholders of unprofitable companies usually expect strong revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

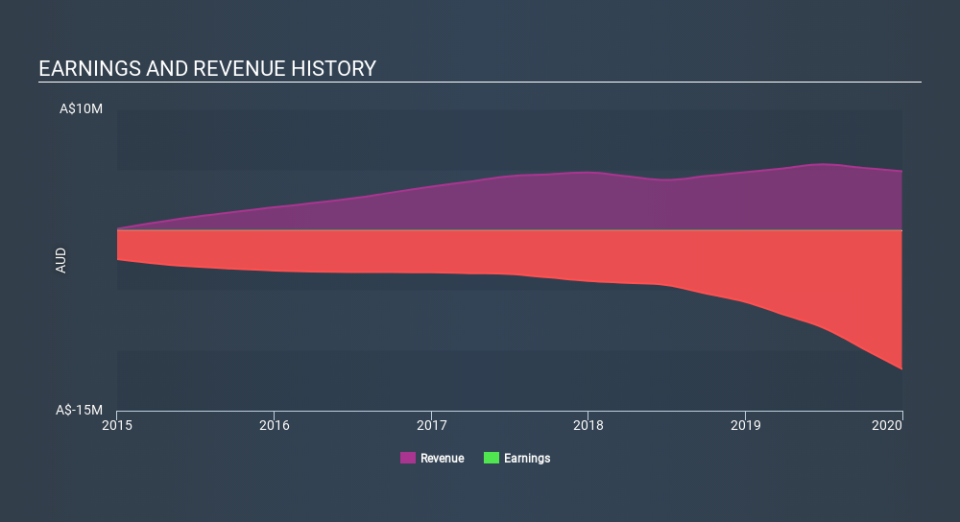

Over three years, Medlab Clinical grew revenue at 9.0% per year. That's a pretty good rate of top-line growth. So it's hard to believe the share price decline of 37% per year is due to the revenue. More likely, the market was spooked by the cost of that revenue. This is exactly why investors need to diversify - even when a loss making company grows revenue, it can fail to deliver for shareholders.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

Take a more thorough look at Medlab Clinical's financial health with this free report on its balance sheet.

A Different Perspective

Medlab Clinical shareholders are down 41% for the year, falling short of the market return. Meanwhile, the broader market slid about 9.5%, likely weighing on the stock. The three-year loss of 37% per year isn't as bad as the last twelve months, suggesting that the company has not been able to convince the market it has solved its problems. We would be wary of buying into a company with unsolved problems, although some investors will buy into struggling stocks if they believe the price is sufficiently attractive. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Take risks, for example - Medlab Clinical has 7 warning signs (and 2 which can't be ignored) we think you should know about.

For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.