Yahoo Finance

Yahoo Finance Here's Why Hydrix (ASX:HYD) Can Afford Some Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Hydrix Limited (ASX:HYD) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Hydrix

What Is Hydrix's Net Debt?

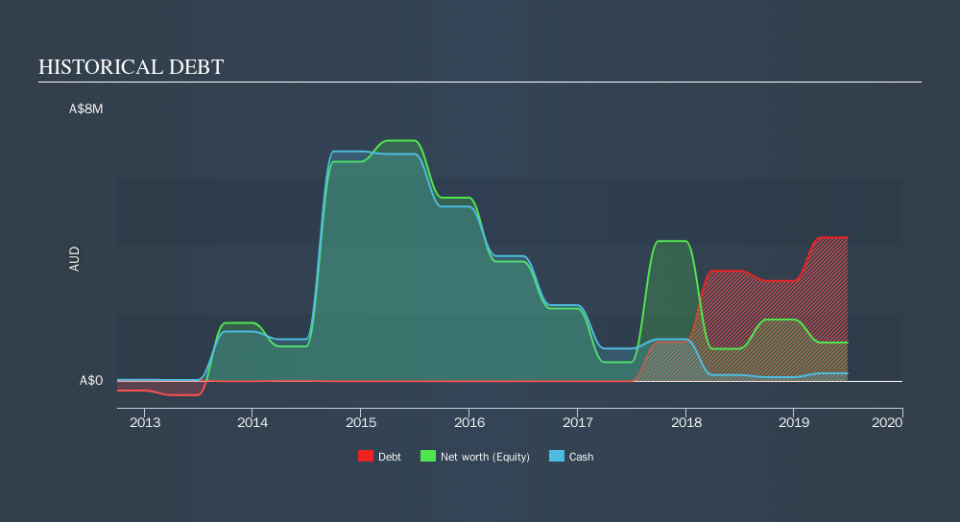

The image below, which you can click on for greater detail, shows that at June 2019 Hydrix had debt of AU$4.23m, up from AU$3.25m in one year. On the flip side, it has AU$234.6k in cash leading to net debt of about AU$4.00m.

How Strong Is Hydrix's Balance Sheet?

We can see from the most recent balance sheet that Hydrix had liabilities of AU$10.1m falling due within a year, and liabilities of AU$1.60m due beyond that. Offsetting these obligations, it had cash of AU$234.6k as well as receivables valued at AU$6.65m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by AU$4.79m.

This deficit isn't so bad because Hydrix is worth AU$20.7m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. When analysing debt levels, the balance sheet is the obvious place to start. But it is Hydrix's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Hydrix reported revenue of AU$14m, which is a gain of 148%, although it did not report any earnings before interest and tax. So its pretty obvious shareholders are hoping for more growth!

Caveat Emptor

Despite the top line growth, Hydrix still had negative earnings before interest and tax (EBIT), over the last year. Indeed, it lost a very considerable AU$3.5m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled AU$4.2m in negative free cash flow over the last twelve months. So in short it's a really risky stock. For riskier companies like Hydrix I always like to keep an eye on whether insiders are buying or selling. So click here if you want to find out for yourself.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.