Yahoo Finance

Yahoo Finance Here's Why Byline Bancorp (NYSE:BY) Has Caught The Eye Of Investors

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

In contrast to all that, many investors prefer to focus on companies like Byline Bancorp (NYSE:BY), which has not only revenues, but also profits. Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Byline Bancorp with the means to add long-term value to shareholders.

See our latest analysis for Byline Bancorp

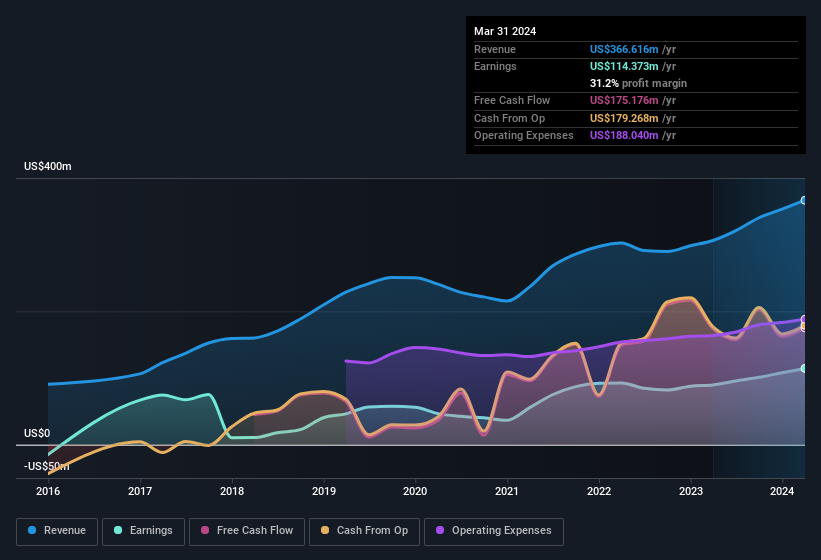

How Fast Is Byline Bancorp Growing?

Generally, companies experiencing growth in earnings per share (EPS) should see similar trends in share price. That means EPS growth is considered a real positive by most successful long-term investors. Impressively, Byline Bancorp has grown EPS by 21% per year, compound, in the last three years. If the company can sustain that sort of growth, we'd expect shareholders to come away satisfied.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. It's noted that Byline Bancorp's revenue from operations was lower than its revenue in the last twelve months, so that could distort our analysis of its margins. While we note Byline Bancorp achieved similar EBIT margins to last year, revenue grew by a solid 20% to US$367m. That's progress.

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

The trick, as an investor, is to find companies that are going to perform well in the future, not just in the past. While crystal balls don't exist, you can check our visualization of consensus analyst forecasts for Byline Bancorp's future EPS 100% free.

Are Byline Bancorp Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

While Byline Bancorp insiders did net US$1.5m selling stock over the last year, they invested US$2.2m, a much higher figure. An optimistic sign for those with Byline Bancorp in their watchlist. Zooming in, we can see that the biggest insider purchase was by Lead Independent Director Antonio Del Valle Perochena for US$433k worth of shares, at about US$21.63 per share.

The good news, alongside the insider buying, for Byline Bancorp bulls is that insiders (collectively) have a meaningful investment in the stock. Indeed, they have a considerable amount of wealth invested in it, currently valued at US$356m. Coming in at 34% of the business, that holding gives insiders a lot of influence, and plenty of reason to generate value for shareholders. Looking very optimistic for investors.

While insiders are apparently happy to hold and accumulate shares, that is just part of the big picture. The cherry on top is that the CEO, Roberto Herencia is paid comparatively modestly to CEOs at similar sized companies. For companies with market capitalisations between US$400m and US$1.6b, like Byline Bancorp, the median CEO pay is around US$3.4m.

The Byline Bancorp CEO received US$2.7m in compensation for the year ending December 2023. That seems pretty reasonable, especially given it's below the median for similar sized companies. CEO compensation is hardly the most important aspect of a company to consider, but when it's reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. It can also be a sign of good governance, more generally.

Should You Add Byline Bancorp To Your Watchlist?

If you believe that share price follows earnings per share you should definitely be delving further into Byline Bancorp's strong EPS growth. Furthermore, company insiders have been adding to their significant stake in the company. These things considered, this is one stock worth watching. You should always think about risks though. Case in point, we've spotted 4 warning signs for Byline Bancorp you should be aware of, and 1 of them can't be ignored.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Byline Bancorp, you'll probably love this curated collection of companies in the US that have an attractive valuation alongside insider buying in the last three months.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.