Yahoo Finance

Yahoo Finance

Here's where Aussie property markets are heading now

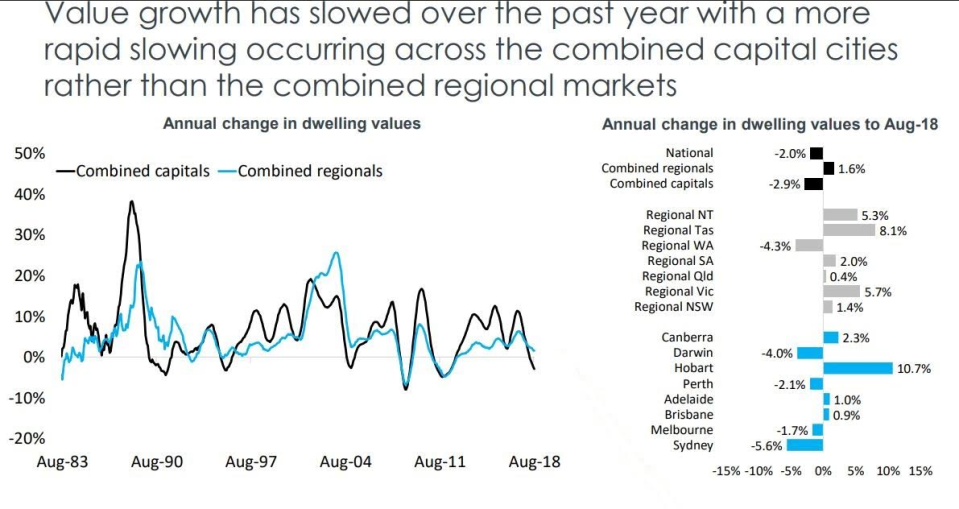

Those of the media outlets who tell us our property market is “collapsing” when in reality values have fallen a total of 2% over the last year.

Also read: Is this Australia’s biggest tax scandal?

Or our new treasurer, Josh Frydenberg, who after consulting with the RBA and APRA has concluded that we’re in for an “orderly” soft landing in the Sydney and Melbourne markets.

Now I’m not suggesting property values won’t fall further in some locations – they will, but there is no sign of a general market collapse.

Also read: Want to be rich and successful? Here’s how

The current tight lending criteria and subdued consumer confidence will continue to weigh heavily on the market, but recently ANZ Bank suggested that there are signs the property markets could stabilise by year end.

So let’s take a look at what’s really happening around the Australian property markets as we unpack the latest Corelogic charts and stats:

Source: Corelogic

Over the last year property values have trended higher in Hobart, Canberra, Adelaide and Brisbane; but are lower in Perth, Darwin, Sydney and Melbourne. In general the more expensive properties, which are more subject to discretionary spending, are the weakest segment of the market.

Source: Corelogic

SYDNEY HOUSING MARKET

The Sydney property market peaked in mid 2017 and home prices are down 5.6% over the last year.

Over the past five years, median dwelling prices have increased by 51.0% compared to household incomes increasing by just 16.1%.

It has been a similar story over the past decade with median price growth (89.0%) more than double the household income growth (42.0% meaning housing affordability has become an issue for some segments of the market.

Sydney is currently offering investors an opportunity to buy established apartments in the eastern suburbs, lower north shore and inner west in a “buyer’s market” with little further downside and the prospect of the market moving forward again in 2019.

MELBOURNE HOUSING MARKET

The Melbourne property market peaked in November 2017 and is experiencing a soft landing after 5 years of strong price growth.

Property values are now 3.5% below their peak.

Over the past five years, median property prices in Melbourne have increased by 41.5% and over the past decade they are 77.3% higher.

By comparison, household incomes are just 12.4% higher over the past five years and 34.7% higher over the decade, both of which are much lower than price growth, meaning housing affordability has become an issue for some segments of the market.

While Melbourne’s property prices are likely to fall by a little further, they will be underpinned by a robust economy, jobs growth Australia’s strongest population growth and the influx of 35% of all overseas migrants.

BRISBANE HOUSING MARKET

Property price growth in Brisbane has been slow over the past few years, however Brisbane is the market with the most potential for growth over the next 3 years.

Housing is relatively affordable in Brisbane compared to the other east coast capital cities.

Over the past five years, median prices are 16.1% higher while household incomes have increased 9.2%.

Throughout the 10 years to June 2018, prices are 24.1% higher while household income growth has been stronger at 31.3%.

Queensland has led the nation in net interstate migration over the past year and job creation is quite strong in part because of the many significant infractructure projects being built.

ADELAIDE HOUSING MARKET

The annual rate of property price growth continues to slow in Adelaide, but prices are up 1% over the last 12 months, a better result that in some other capital cities.

The greatest price growth has shifted from the highest valued properties towards the lower and middle of the market.

But the 12.5% increase in new unit supply expected over the next two years is likely to put a dampener on the market.

With little price growth occurring housing remains relatively affordable in Adelaide.

Over the past 5 years dwelling prices are 15.6% higher compared to an 11.9% increase in household income growth.

Over the past decade total house price growth (31.6%) and the growth in household incomes has been very similar.

I know some investors are looking for opportunities in Adelaide hoping (“speculating”) prices will increase but there are few growth drivers in Adelaide which is experiencing above average unemployment rates and poor employment growth.

PERTH HOUSING MARKET

The Perth property market has been on a downward trajectory since peaking in June 2014.

For a brief period earlier in the year, Perth’s housing market was showing some positive signs, however values have trended lower over the past four months to be down 2.3% over the first eight months of the year.

The local unit market has recorded weaker conditions relative to houses, with unit values down 5.5% over the year to date while house values are down a lower 1.5%.

Prices and rents have been falling in Perth since 2014 and as a result there has been a substantial improvement in housing affordability.

Household income has grown at a faster pace over the past five (3.7%) and 10 years (30.6%) than median dwelling prices over the past five (1.1%) and 10 years (11.6%) leading to a significant improvement in affordability, yet Perth house prices keep falling due to local economic conditions, poor consumer confidence and an adverse supply and demand ratio.

While the Perth market may level out in the next six months, it’s much too early for a countercyclical investment in the west – I can’t see prices rising significantly for a number of years.

HOBART MARKET UPDATE

Hobart has been the strongest performing capital city over the last 2 years.

Over the last five years median dwelling prices have increased at about double the rate of household income growth creating a deterioration in housing affordability in the Apple Isle.

This together with investors moving their aim to the next “hot spot” suggests that Hobart’s strong property price growth will slow down in the coming year.

DARWIN HOUSING MARKET

The Darwin property market peaked in August 2010 is still suffering from the effects of the end of our mining boom today 8 years later falling a another 4% over the last year, and our research suggests that house prices are likely to keep falling for some time yet.

Darwin is Australia’s most affordable capital city housing markets due to its high wages at a time of continuing house price and rental falls.

Over the past decade, prices are up 30.3% compared to a 60.8% increase in household incomes.

Darwin does not have significant growth drivers on the horizon and would be best avoided by investors.

CANBERRA MARKET UPDATE

Canberra’s property market is a “quiet achiever” having grown 3.4 % over the last year and is likely to continue to perform well underpinned by a stable economy which has led to steady employment and to above average population growth (1.8% per annum.)

Houses price growth has outpaced its flatter apartment market.

Housing affordability in Canberra has deteriorated over the past five years, as median house prices grew 23.6% during a period when household incomes only grew 15.5%.

Interestingly over the past decade, median prices have increased at a similar rate (40.0%) to household incomes (41.4%).

RENTAL GROWTH HAS STALLED

At the same time as house prices are fallen rental growth has been sluggish around Australia, and rents have fallen a little in Sydney and Darwin.

Another sign of our slowing markets is the increased length of time it takes to sell a property with the length of time it takes to sell a property having increased relative to a year ago.

POPULATION GROWTH

Population growth remains strong however, and this will underpin our property markets.

THE BOTTOM LINE…

We’re clearly in the next stage of the property cycle and Australia’s property markets are very fragmented, driven by local factors including jobs growth, population growth, consumer confidence and supply and demand.

This makes it an opportune time for both home buyers and investors to buy property at a time when they’ll face less competition.

However correct asset selection will be more important now than ever, so only buy in areas where there are multiple growth drivers such as employment growth, population growth or major infrastructure changes.

Similarly, suburbs undergoing gentrification are likely to outperform.

Michael Yardney is a director of Metropole Property Strategists, which creates wealth for its clients through independent, unbiased property advice and advocacy. He is a best-selling author, one of Australia’s leading experts in wealth creation through property and writes the Property Update blog.