Yahoo Finance

Yahoo Finance If You Had Bought Hillenbrand (NYSE:HI) Stock A Year Ago, You'd Be Sitting On A 46% Loss, Today

Passive investing in an index fund is a good way to ensure your own returns roughly match the overall market. But if you buy individual stocks, you can do both better or worse than that. Investors in Hillenbrand, Inc. (NYSE:HI) have tasted that bitter downside in the last year, as the share price dropped 46%. That contrasts poorly with the market return of 1.1%. Longer term shareholders haven't suffered as badly, since the stock is down a comparatively less painful 14% in three years. Furthermore, it's down 29% in about a quarter. That's not much fun for holders.

View our latest analysis for Hillenbrand

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

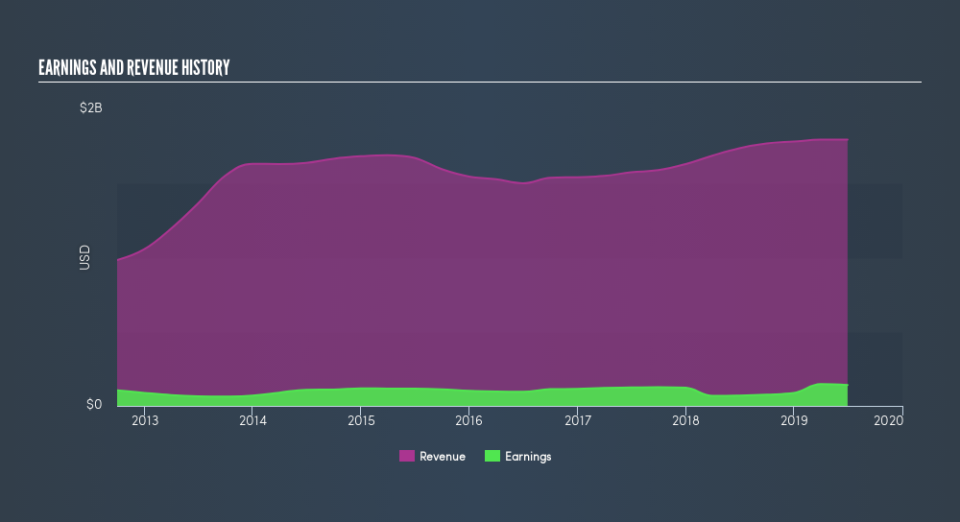

Even though the Hillenbrand share price is down over the year, its EPS actually improved. Of course, the situation might betray previous over-optimism about growth. It's fair to say that the share price does not seem to be reflecting the EPS growth. But we might find some different metrics explain the share price movements better.

Hillenbrand's revenue is actually up 3.3% over the last year. Since the fundamental metrics don't readily explain the share price drop, there might be an opportunity if the market has overreacted.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

We know that Hillenbrand has improved its bottom line lately, but what does the future have in store? This free report showing analyst forecasts should help you form a view on Hillenbrand

What about the Total Shareholder Return (TSR)?

Investors should note that there's a difference between Hillenbrand's total shareholder return (TSR) and its share price change, which we've covered above. Arguably the TSR is a more complete return calculation because it accounts for the value of dividends (as if they were reinvested), along with the hypothetical value of any discounted capital that have been offered to shareholders. Dividends have been really beneficial for Hillenbrand shareholders, and that cash payout explains why its total shareholder loss of 45%, over the last year, isn't as bad as the share price return.

A Different Perspective

Hillenbrand shareholders are down 45% for the year (even including dividends), but the market itself is up 1.1%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 1.0% per year over five years. We realise that Buffett has said investors should 'buy when there is blood on the streets', but we caution that investors should first be sure they are buying a high quality businesses. Importantly, we haven't analysed Hillenbrand's dividend history. This free visual report on its dividends is a must-read if you're thinking of buying.

We will like Hillenbrand better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.