Yahoo Finance

Yahoo Finance Gold Up And Dollar Down As The Fed Stays Firm

Gold has continued to make gains over the last few days while the US dollar has mostly continued its decline against other major currencies. Wednesday’s minutes from the Federal Reserve (‘the Fed’) don’t contain much new information but they do underline determination to avoid a resurgence of inflation which might occur if rates are cut too quickly. This article summarises recent news and sentiment on the American economy and looks briefly at the charts of gold and euro-dollar.

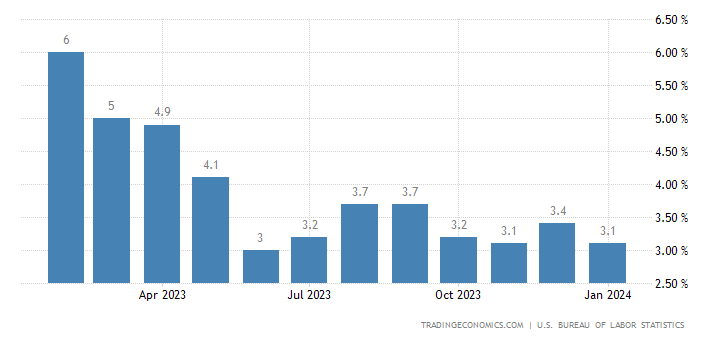

The Fed’s latest minutes seem to confirm that the terminal rate of this cycle has been reached, something already seen as more-or-less certain by most participants. However, the first expected cut has been pushed further back to June. CME FedWatch Tool gives a probability of about 70% that there will be at least one cut by 12 June. Senior members of the Fed want to see a further sustained reduction in inflation before seriously considering looser policy. This hasn’t come yet, although there doesn’t seem to be strong residual inflationary pressure for the moment either:

Expectations of a decline below 3% last month for the first time in years were unmet, although the result of 3.1% was only 0.2% higher than the consensus. As in various other major, advanced economies, a tight labour market and rising earnings continue to put some pressure on prices in the USA, even as rates of inflation from fuel and supply chains have declined strongly since 2022.

Overall, the situation for the economy in the USA seems to be much better than the rest of the top 10. There’s definitely no indication whatsoever of recession from GDP data:

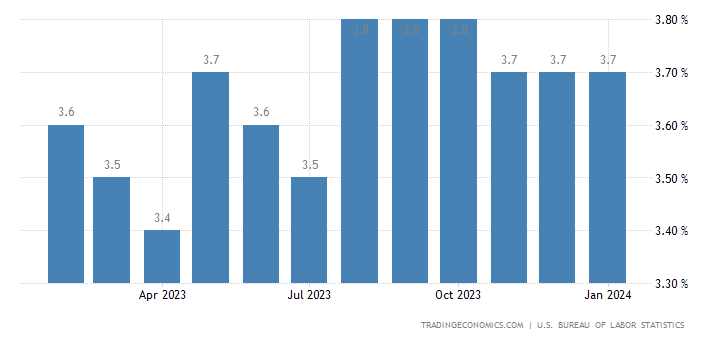

On the contrary, growth improved strongly in the third quarter of last year, much more than expected, and preliminary data for Q4 were also significantly higher than the consensus of 2%. Consumer spending seems to have slowed slightly last quarter compared to Q3, but that’s partially a function of the particularly large gain in Q3. The job market also seems to be generally strong:

Unemployment of 3.7% is close to all-time lows, which is significant in the context of rates having risen so high so quickly. Equally, there’s no sign of a significant uptick in unemployment since last year; the rate has been mostly consistent since early 2022.

Overall, there’s no strong pressure on the Fed to start cutting rates at the soonest to avoid a recession or even a ‘necessarily economic slowdown’. That’s certainly positive for the average American and for most investors around the world, but for traders it creates various questions. It’s difficult to see what fundamental factor can push gold much further up as rates are almost certain to remain higher than inflation for the whole year. Equally, it might seem strange that the dollar hasn’t reacted more strongly to recent news of higher rates for longer.

Gold, Daily

Gold has recovered steadily since the significant drop around inflation on 13 February. Now that the price is within the value area between the 50 and 100 SMAs, it might consolidate for a while before resuming gains around the next important release. There’s no sign of saturation from either the slow stochastic or Bollinger Bands. Although the long-term trend from the weekly chart is upward, on D1 it’s sideways since December.

That makes the most likely scenario in the near future consolidation within a shrinking range. Next week the focus is on second estimate GDP on Wednesday followed by personal consumption expenditures and personal income and spending on Thursday. These probably won’t have as big an effect on markets as inflation or the NFP but traders should remain alert to the possibility of a fakeout upward if the releases are surprising.

Euro-dollar, Daily

Now that both the Fed and the ECB are expected by small majorities to start cutting in June, the playing field for euro-dollar is a bit more level. Although economic conditions in the eurozone are on the whole much more challenging than in the USA, there’s no evidence of a serious recession anywhere in Europe. On the chart, the main potential concern for a possible buyer is that the recent bounce seems a bit too sharp.

At the time of writing, the 50 SMA is still a possibly important resistance which might drive a rejection lower given the size of the current period’s wick; however, completion should be awaited to assess the validity of this idea better. If the price does move down from here, though, there might be a retest of recent lows around $1.07. The most important release affecting the euro next week is inflation on Friday; national inflation from France, Germany and Italy are also coming up on Thursday 29 February and Friday 1 March.

The opinions in this article are personal to the writer. They do not reflect those of Exness or FX Empire.

This article was originally posted on FX Empire