Yahoo Finance

Yahoo Finance Domino's (DPZ) Beats on Q3 Earnings, Lowers Long-term View

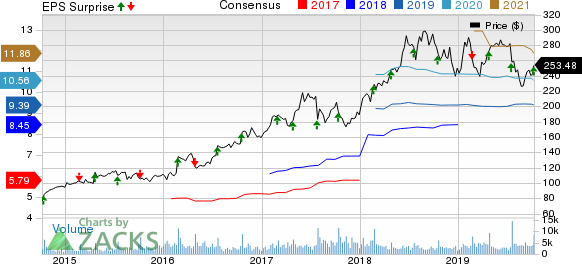

Domino's Pizza, Inc. DPZ reported mixed third-quarter 2019 financial numbers, wherein earnings surpassed the Zacks Consensus Estimate but revenues came almost in line with the same. Notably, this marked the company’s third straight quarter of earnings beat. However, the company reported disappointing same-store sales. Domino's also lowered its long-term view.

Despite lowering its long-term guidance, shares of the company gained 4.7% yesterday as a new $1 billion share repurchase program provided cushion to the stock. Year to date, Domino's has gained 2.2% compared with the industry’s 23.7% growth.

Adjusted earnings in the quarter under review came in at $2.05 per share, which outpaced the Zacks Consensus Estimate of $2.04. The metric also increased 5.1% on a year-over-year basis. The bottom-line improvement was driven by higher net income, overshadowed by a higher effective tax rate.

Quarterly revenues improved 4.4% year over year to $820.8 million, which came almost in line with the consensus mark of $821 million. Higher supply chain volume, increase in same-store sales and in-store count both in the United States and international markets drove the company’s revenues. International franchise revenues also increased but were marginally overshadowed by foreign currency headwinds.

However, the company-owned store revenues declined in the quarter due to the sale of 59 U.S. company-owned stores to existing U.S. franchisees.

Domino's Pizza Inc Price, Consensus and EPS Surprise

Domino's Pizza Inc price-consensus-eps-surprise-chart | Domino's Pizza Inc Quote

Comps

Global retail sales (including total sales of franchise and company-owned units) rose 5.8% year over year in the third quarter. This compared unfavorably with 8.3% growth registered in the year-ago quarter. The uptick can be attributed to solid comps at international stores (up 5.7%) and domestic stores (up 6%). Excluding foreign currency impact, global retail sales increased 7.5%.

In the third quarter, comps at Domino’s domestic stores (including company-owned and franchise stores) improved 2.4%. This compared unfavorably with a 6.3% increase in the year-ago quarter.

At domestic company-owned stores, Domino’s comps grew 1.7% year over year, lower than 4.9% registered in the year-ago quarter. Also, domestic franchise stores comps increased 2.5% compared with a 6.4% rise in third-quarter 2018.

Comps at international stores, excluding foreign currency translation, were up 1.7%. This was comparatively lower than the 3.3% increase recorded in the year-ago quarter.

Notably, the third quarter marked the 34th consecutive quarter of positive U.S. comparable sales and the 103rd consecutive quarter of positive international comps.

Margins

Domino’s operating margin expanded 90 basis points (bps) year over year to 38.5% in the reported quarter. Operating margin expansion was driven by a rise in supply chain margin owing to the positive impact of procurement savings as well as lower insurance costs. Moreover, the net income margin expanded 40 bps to 11%.

Balance Sheet

As of Sep 8, 2019, cash and cash equivalents totaled $66.7 million, up from $25.4 million as of Dec 30, 2018. Long-term debt at the end of the third quarter was $3,407.1 million, down from $3,495.7 million as of Dec 30, 2018. Inventory amounted to $51 million at the end of the third quarter.

Cash flows from operating activities summed $324.6 million as of Sep 8, 2019. In the quarter under review, Domino’s has spent $42.7 million on capital expenditures.

Long-term View

Domino’s has lowered its long-range outlook from three- to five-year to two- to three-year. The company now expects global retail sales growth of 7-10% in two- to three-year period, compared with the prior guidance of 8-12% in three- to five-year period. The company expects same-store sales growth in the range of 2-5% in two- to three-year period compared with earlier guided range of 3-6% in three- to five-year period. International same-store sales growth is anticipated to be in the range of 1-4% in two- to three-year period, lower than the earlier provided range of 3-6% in three- to five-year period.

Zacks Rank & Stocks to Consider

Domino’s carries a Zacks Rank #3 (Hold). Better-ranked stocks in the same space include Brinker International, Inc. EAT, Chipotle Mexican Grill, Inc. CMG and Cracker Barrel Old Country Store, Inc. CBRL, each carrying a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Brinker International, Chipotle Mexican Grill and Cracker Barrel Old Country Store have an impressive long-term earnings growth rate of 5.9%, 18.4% and 9.5%, respectively.

Today's Best Stocks from Zacks

Would you like to see the updated picks from our best market-beating strategies? From 2017 through 2018, while the S&P 500 gained +15.8%, five of our screens returned +38.0%, +61.3%, +61.6%, +68.1%, and +98.3%.

This outperformance has not just been a recent phenomenon. From 2000 – 2018, while the S&P averaged +4.8% per year, our top strategies averaged up to +56.2% per year.

See their latest picks free >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Domino's Pizza Inc (DPZ) : Free Stock Analysis Report

Chipotle Mexican Grill, Inc. (CMG) : Free Stock Analysis Report

Brinker International, Inc. (EAT) : Free Stock Analysis Report

Cracker Barrel Old Country Store, Inc. (CBRL) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research