Yahoo Finance

Yahoo Finance Did Fluence's (ASX:FLC) Share Price Deserve to Gain 30%?

Want to participate in a research study? Help shape the future of investing tools and earn a $60 gift card!

Vanguard founder Jack Bogle helped spearhead the low-cost index fund, putting average returns within reach of every investor. But you can make superior returns by picking better-than average stocks. Notably, the Fluence Corporation Limited (ASX:FLC) share price has gained 30% in three years, which is better than the average market return. Zooming in, the stock is up just 1.0% in the last year.

See our latest analysis for Fluence

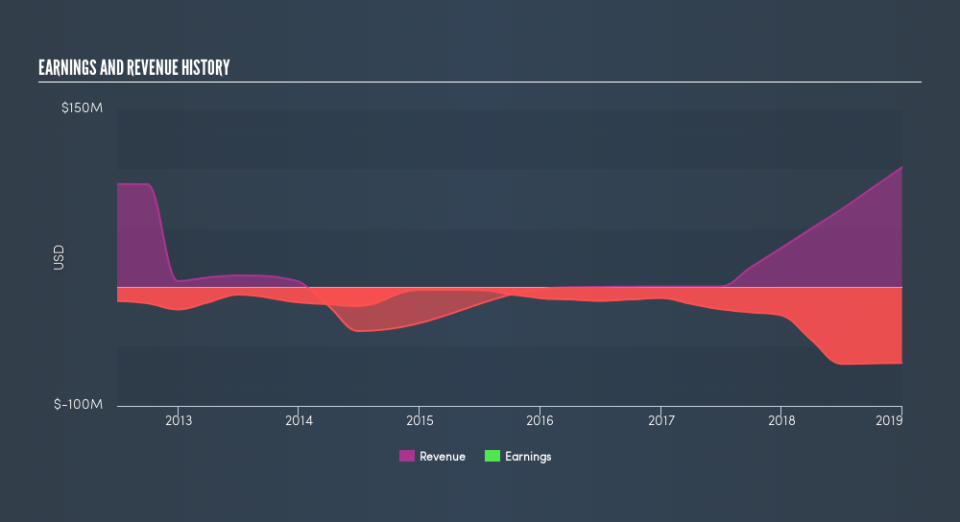

Fluence isn't a profitable company, so it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. When a company doesn't make profits, we'd generally expect to see good revenue growth. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

Over the last three years Fluence has grown its revenue at 127% annually. That's much better than most loss-making companies. The share price rise of 9.2% per year throughout that time is nice to see, and given the revenue growth, that gain seems somewhat justified. If that's the case, now might be the time to take a close look at Fluence. A window of opportunity may reveal itself with time, if the business can trend to profitability.

You can see how revenue and earnings have changed over time in the image below, (click on the chart to see cashflow).

It's good to see that there was some significant insider buying in the last three months. That's a positive. On the other hand, we think the revenue and earnings trends are much more meaningful measures of the business. So it makes a lot of sense to check out what analysts think Fluence will earn in the future (free profit forecasts)

A Different Perspective

Fluence shareholders are up 1.0% for the year. But that return falls short of the market. But at least that's still a gain! Over five years the TSR has been a reduction of 6.0% per year, over five years. It could well be that the business is stabilizing. It is all well and good that insiders have been buying shares, but we suggest you check here to see what price insiders were buying at.

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.