Yahoo Finance

Yahoo Finance Buru Energy (ASX:BRU) shareholders have endured a 46% loss from investing in the stock three years ago

As an investor its worth striving to ensure your overall portfolio beats the market average. But the risk of stock picking is that you will likely buy under-performing companies. We regret to report that long term Buru Energy Limited (ASX:BRU) shareholders have had that experience, with the share price dropping 46% in three years, versus a market decline of about 12%. The falls have accelerated recently, with the share price down 19% in the last three months. But this could be related to the weak market, which is down 13% in the same period.

So let's have a look and see if the longer term performance of the company has been in line with the underlying business' progress.

See our latest analysis for Buru Energy

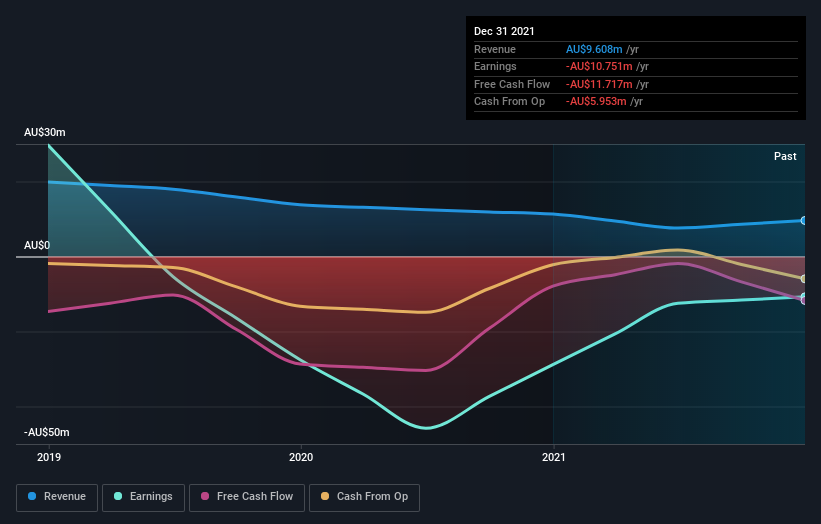

Buru Energy isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. When a company doesn't make profits, we'd generally expect to see good revenue growth. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

In the last three years Buru Energy saw its revenue shrink by 30% per year. That means its revenue trend is very weak compared to other loss making companies. With revenue in decline, the share price decline of 14% per year is hardly undeserved. The key question now is whether the company has the capacity to fund itself to profitability, without more cash. The company will need to return to revenue growth as quickly as possible, if it wants to see some enthusiasm from investors.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

Take a more thorough look at Buru Energy's financial health with this free report on its balance sheet.

A Different Perspective

While it's never nice to take a loss, Buru Energy shareholders can take comfort that their trailing twelve month loss of 6.5% wasn't as bad as the market loss of around 8.4%. Unfortunately, last year's performance may indicate unresolved challenges, given that it's worse than the annualised loss of 2% over the last half decade. While some investors do well specializing in buying companies that are struggling (but nonetheless undervalued), don't forget that Buffett said that 'turnarounds seldom turn'. It's always interesting to track share price performance over the longer term. But to understand Buru Energy better, we need to consider many other factors. Take risks, for example - Buru Energy has 4 warning signs (and 1 which is a bit unpleasant) we think you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.