Yahoo Finance

Yahoo Finance Bank of America (BAC) Falls 14.1% YTD: Will it Rebound Soon?

Amid the ongoing regional banking crisis, investors are turning bearish on the stocks. Apart from the recession fear, deposit outflows are a big drag on the banks. The KBW Nasdaq Bank Index is down 23.5% so far this year on investors’ pessimistic stance on the sector. On the other hand, the S&P 500 Index is trading in green.

So, investors must look for stocks that are fundamentally well-placed and will continue to thrive once the current headwinds cool off. Today we will be discussing one of the largest banks in the United States — Bank of America BAC — which is down 14.1% so far this year.

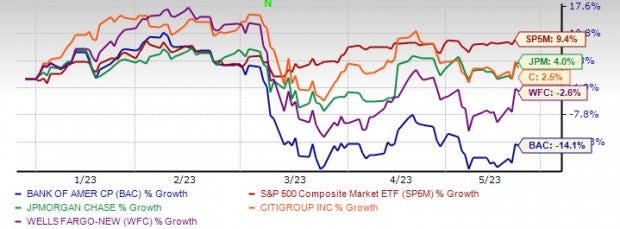

This Zacks Rank #3 (Hold) stock has underperformed Wells Fargo WFC, JPMorgan JPM and Citigroup C as well. In the year-to-date period, WFC has declined 2.6%, while JPM and C gained 4% and 2.6%, respectively. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Year-to-Date Price Performance

Image Source: Zacks Investment Research

One of the reasons for investor apathy toward Bank of America seems to be its highly asset-sensitive balance sheet. Last year, the company recorded a 22% jump in net interest income (NII) (FTE) as the Federal Reserve raised the interest rates to a 15-year high of 4.25-4.50% to curb inflation. This was also supported by robust loan growth.

The uptrend in both NII (FTE) and loans continued in the first quarter as well. But now the company expects the rise in funding costs and modest loan growth to weigh on NII in the upcoming quarters. Management expects NII (FTE) to be roughly $14.3 billion in the second quarter of 2023. For the full year, the metric is projected to grow 7-8%.

Other than this, the deteriorating operating environment is a major near-term headwind.

Despite these concerns, Bank of America is fundamentally strong. Let’s discuss factors that show that the stock is worth keeping an eye on despite the recent sell-off.

Attractive Valuation: At $28.47 per share, Bank of America is currently trading at a price/tangible book value of 1.28X, way below the broader market average of 9.90X. Thus, the company’s beaten-down stock price and attractive valuation might be a good entry point for investors.

Price-to-Tangible Book Ratio (TTM)

Image Source: Zacks Investment Research

Robust Fundamental Growth Drivers: Bank of America continues to align its banking center network according to customer needs. These initiatives, along with the success of Zelle and Erica, have enabled it to improve digital offerings and cross-sell several products, including mortgages, auto loans and credit cards. The acquisition of Axia Technologies strengthened its healthcare payments business.

BAC remains focused on acquiring the industry's best deposit franchise and strengthening the loan portfolio. Despite a challenging operating environment, deposits and loan balances have remained solid over the past several years. Though loan demand has remained subdued since the pandemic, the same is witnessing a decent increase of late. As of Mar 31, 2023, total loans and leases grew 5.4% year over year to $1.05 trillion. While tightening of the monetary policy and rising recession risk are the headwinds, the demand for loans is expected to remain decent in the quarters ahead.

Improved Capital Deployments: Following the clearance of the 2022 stress test, BAC raised the quarterly dividend by 5% to 22 cents per share. Prior to this, the company had announced a 17% hike to its quarterly dividend in July 2021.

In October 2021, the company's share repurchase plan of $25 billion was renewed. In the first quarter of 2023, it returned $4 billion to shareholders in the form of buybacks and dividend payouts. Driven by a strong capital position and earnings strength, the company is expected to sustain improved capital deployments and enhance shareholder value.

Favorable Estimate Revision & Surprise History: Analysts seem bullish on the stock. Over the past month, the Zacks Consensus Estimate for earnings has moved 4% north for 2023. Its projected long-term earnings per share growth rate is 7%.

Bank of America has an impressive earnings surprise history. The company outpaced estimates in three of the trailing four quarters, the average earnings surprise being 7.04%.

Conclusion

Considering Bank of America’s growth prospects and robust fundamentals, investors must watch the stock for long-term gains. The company’s efforts to improve revenues, strong balance sheet and liquidity positions and expansion into new markets will keep aiding its financials. So, once the near-term uncertainty moves away, the stock is likely to regain investor confidence and rally.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bank of America Corporation (BAC) : Free Stock Analysis Report

Wells Fargo & Company (WFC) : Free Stock Analysis Report

JPMorgan Chase & Co. (JPM) : Free Stock Analysis Report

Citigroup Inc. (C) : Free Stock Analysis Report