Yahoo Finance

Yahoo Finance

'No place to hide': The stock market's sell-off has left investors scrambling for cover

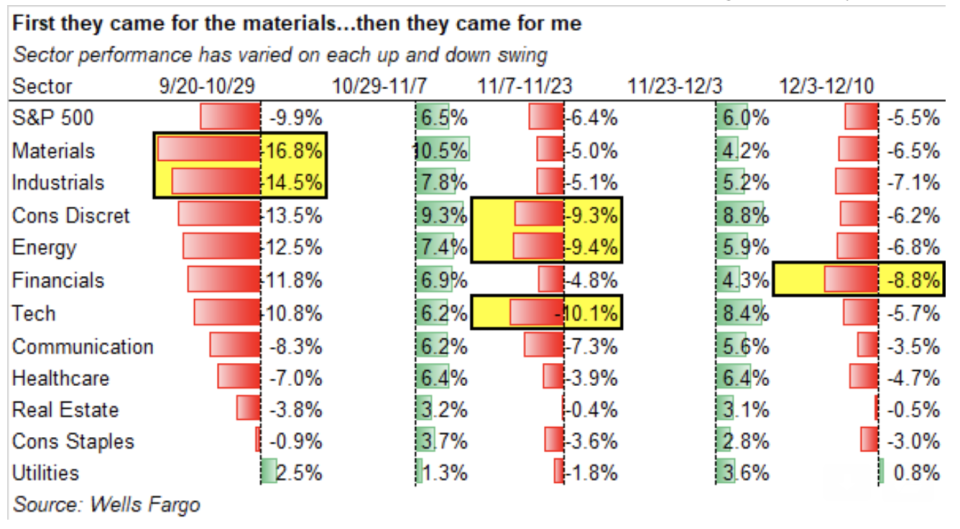

US stocks are set to close out 2018 well off their highs, but each trampled sector's sell-off since the beginning of October has been quite different, according to a Wells Fargo analysis.

The sell-off has been unlike other periods of market turbulence, like in February of this year and August of 2015, a Wells Fargo equity derivatives strategist contends.

Low stock correlation - individual stocks moving out of sync with one another, rather than in tandem - has been the primary reason for that, the strategist found.

The market's sell-off since the beginning of October has left investors with few places to hide.

Underneath the market's surface, each sector has undergone starkly different declines at different periods, according to a newly released Wells Fargo analysis pinpointing low stock correlation - individual stocks moving out of sync with one another, rather than in tandem - as the primary reason for the uneven price action.

"Although the S&P has been churning in a 2600-2800 range, there's more going on under the surface," Pravit Chintawongvanich, equity derivatives strategist at the firm, wrote in a note to clients on Tuesday morning.

"In the initial selloff, materials/industrials did the worst. In the second selloff, energy & tech/FANG did the worst. In the third selloff, financials did the worst. There's been 'no place to hide' as each favourite long eventually had its number called."

The sell-off since the market's top in late September/early October has been fuelled in part by uncertainty around the US-China trade war, rising interest rates, and concerns about slowing global growth.

But this carnage has been different than sell-offs in recent history, according to Chintawongvanich, due largely to selling on a stock-specific basis rather than on an index-specific basis ("stock selloff'", not an "index selloff," as he puts it). The single-stock correlation has been drastically lower than in previous notable sell-offs.

"In other words, this is a 'bottoms up' rather than 'top down' selloff," he wrote.

"When futures/index trading dominate the selling, all sectors, even defensives, tend to be uniformly down and long/short strategies typically do OK. ... This time around, defensive sectors have thrived compared to other sectors."

This could also help explain why the S&P 500's expected volatility as measured by the Cboe Volatility Index (the VIX) has been relatively muted. The VIX has traded between 12 and 29 since the start of October. By comparison, it traded above 50 during the sell-offs that took place this past February and in August 2015 (the instances Chintawongvanich points out).

Indeed, the sectors managing to keep their heads above water are the traditionally defensive corners of the market. While the S&P 500 has plunged nearly 9% in three months, the utilities sector is up 4% and the consumer staples sector is up about 1%. Healthcare, meanwhile, is down just over 1% during that time, though it is the top-performing sector this year.

"A more mundane reason for unreactive [volatility] could be that the holiday season is coming up," Chintawongvanich said. "Realised volatility has historically dropped during the holiday season as volumes dry up."

Now read: