Yahoo Finance

Yahoo Finance Should You Be Adding Medusa Mining (ASX:MML) To Your Watchlist Today?

Some have more dollars than sense, they say, so even companies that have no revenue, no profit, and a record of falling short, can easily find investors. But as Warren Buffett has mused, 'If you've been playing poker for half an hour and you still don't know who the patsy is, you're the patsy.' When they buy such story stocks, investors are all too often the patsy.

In the age of tech-stock blue-sky investing, my choice may seem old fashioned; I still prefer profitable companies like Medusa Mining (ASX:MML). While profit is not necessarily a social good, it's easy to admire a business that can consistently produce it. While a well funded company may sustain losses for years, unless its owners have an endless appetite for subsidizing the customer, it will need to generate a profit eventually, or else breathe its last breath.

View our latest analysis for Medusa Mining

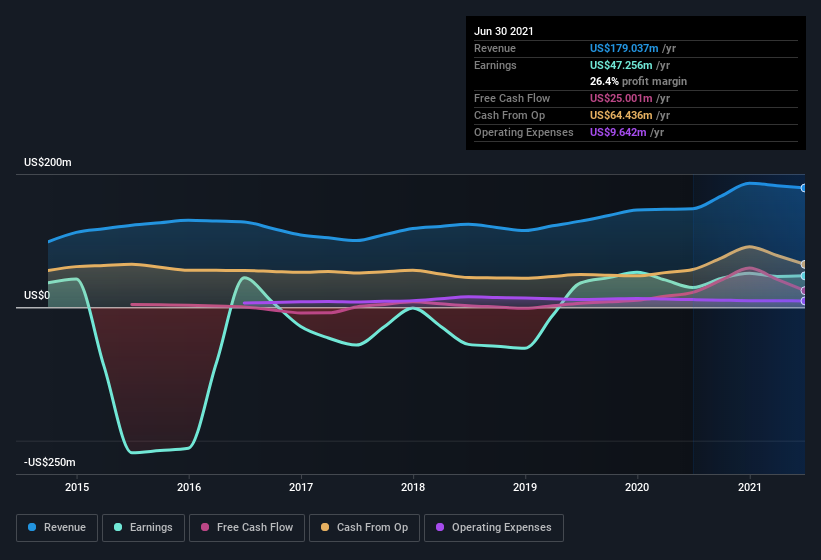

Medusa Mining's Improving Profits

In the last three years Medusa Mining's earnings per share took off like a rocket; fast, and from a low base. So the actual rate of growth doesn't tell us much. Thus, it makes sense to focus on more recent growth rates, instead. Like a falcon taking flight, Medusa Mining's EPS soared from US$0.14 to US$0.23, over the last year. That's a impressive gain of 59%.

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). The good news is that Medusa Mining is growing revenues, and EBIT margins improved by 12.9 percentage points to 35%, over the last year. That's great to see, on both counts.

You can take a look at the company's revenue and earnings growth trend, in the chart below. To see the actual numbers, click on the chart.

Since Medusa Mining is no giant, with a market capitalization of AU$171m, so you should definitely check its cash and debt before getting too excited about its prospects.

Are Medusa Mining Insiders Aligned With All Shareholders?

Like the kids in the streets standing up for their beliefs, insider share purchases give me reason to believe in a brighter future. Because oftentimes, the purchase of stock is a sign that the buyer views it as undervalued. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

Not only did Medusa Mining insiders refrain from selling stock during the year, but they also spent US$202k buying it. That puts the company in a nice light, as it makes me think its leaders are feeling confident. It is also worth noting that it was Independent Non-Executive Director Roy Daniel who made the biggest single purchase, worth AU$160k, paying AU$0.87 per share.

Does Medusa Mining Deserve A Spot On Your Watchlist?

For growth investors like me, Medusa Mining's raw rate of earnings growth is a beacon in the night. The growth rate whets my appetite for research, and the insider buying only increases my interest in the stock. So on this analysis I believe Medusa Mining is probably worth spending some time on. Another important measure of business quality not discussed here, is return on equity (ROE). Click on this link to see how Medusa Mining shapes up to industry peers, when it comes to ROE.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Medusa Mining, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.