Yahoo Finance

Yahoo Finance Update: Access Intelligence (LON:ACC) Stock Gained 57% In The Last Five Years

When we invest, we're generally looking for stocks that outperform the market average. And the truth is, you can make significant gains if you buy good quality businesses at the right price. For example, long term Access Intelligence Plc (LON:ACC) shareholders have enjoyed a 57% share price rise over the last half decade, well in excess of the market return of around 6.3% (not including dividends). However, more recent returns haven't been as impressive as that, with the stock returning just 36% in the last year.

View our latest analysis for Access Intelligence

Because Access Intelligence is loss-making, we think the market is probably more focussed on revenue and revenue growth, at least for now. Shareholders of unprofitable companies usually expect strong revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

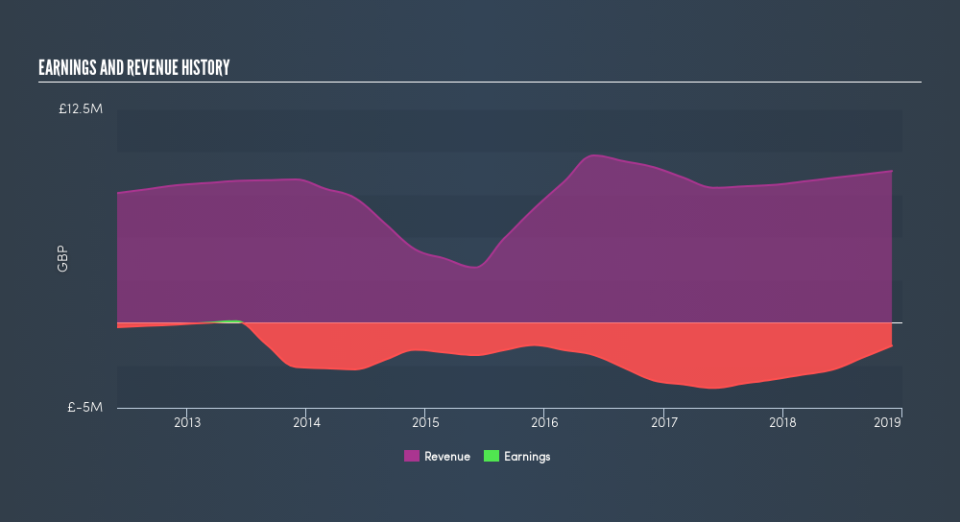

In the last 5 years Access Intelligence saw its revenue grow at 8.3% per year. That's a pretty good long term growth rate. Revenue has been growing at a reasonable clip, so it's debatable whether the share price growth of 9.5% full reflects the underlying business growth. If revenue growth can maintain for long enough, it's likely profits will flow. There's no doubt that it can be difficult to value pre-profit companies.

Depicted in the graphic below, you'll see revenue and earnings over time. If you want more detail, you can click on the chart itself.

Balance sheet strength is crucual. It might be well worthwhile taking a look at our free report on how its financial position has changed over time.

A Different Perspective

It's nice to see that Access Intelligence shareholders have received a total shareholder return of 36% over the last year. That gain is better than the annual TSR over five years, which is 9.5%. Therefore it seems like sentiment around the company has been positive lately. Someone with an optimistic perspective could view the recent improvement in TSR as indicating that the business itself is getting better with time. You could get a better understanding of Access Intelligence's growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Of course Access Intelligence may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on GB exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.