Yahoo Finance

Yahoo Finance 72% earnings growth over 1 year has not materialized into gains for FMC (NYSE:FMC) shareholders over that period

The nature of investing is that you win some, and you lose some. And unfortunately for FMC Corporation (NYSE:FMC) shareholders, the stock is a lot lower today than it was a year ago. The share price has slid 55% in that time. Notably, shareholders had a tough run over the longer term, too, with a drop of 51% in the last three years. More recently, the share price has dropped a further 15% in a month.

Given the past week has been tough on shareholders, let's investigate the fundamentals and see what we can learn.

View our latest analysis for FMC

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

Even though the FMC share price is down over the year, its EPS actually improved. Of course, the situation might betray previous over-optimism about growth.

It's surprising to see the share price fall so much, despite the improved EPS. But we might find some different metrics explain the share price movements better.

We don't see any weakness in the FMC's dividend so the steady payout can't really explain the share price drop. We'd be more worried about the fact that revenue fell 23% year on year. The market may be extrapolating the decline, leading to questions around the sustainability of the EPS.

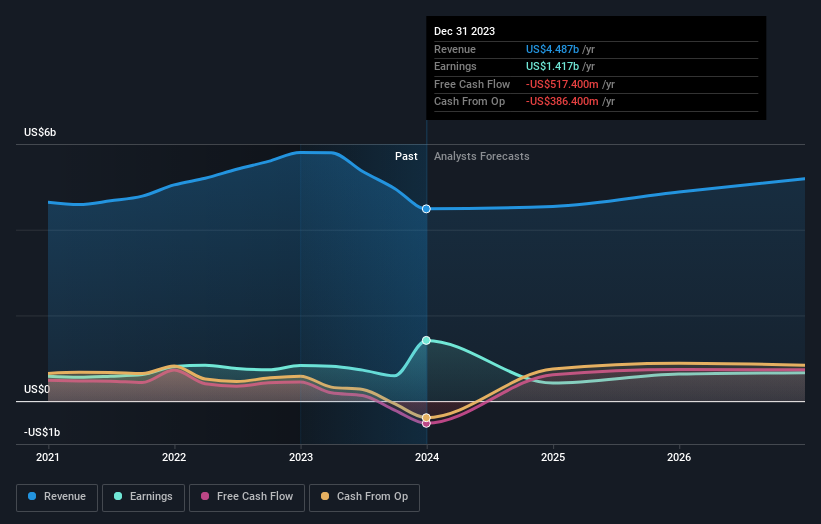

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

It's probably worth noting we've seen significant insider buying in the last quarter, which we consider a positive. That said, we think earnings and revenue growth trends are even more important factors to consider. You can see what analysts are predicting for FMC in this interactive graph of future profit estimates.

A Different Perspective

Investors in FMC had a tough year, with a total loss of 53% (including dividends), against a market gain of about 23%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 4% per year over five years. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For example, we've discovered 4 warning signs for FMC (3 are a bit unpleasant!) that you should be aware of before investing here.

FMC is not the only stock insiders are buying. So take a peek at this free list of growing companies with insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.