Yahoo Finance

Yahoo Finance Zions' (ZION) Solid Loans and Deposits Aid Amid Rising Costs

Zions Bancorp ZION remains well-poised for growth driven by strong loans and deposits, higher interest rates and efforts to boost fee income. However, a mounting expense base and weak asset quality remain headwinds.

Zions remains focused on its organic growth strategy. The company’s total revenues reflected a compound annual growth rate (CAGR) of 2.3% in the last five years ended 2023. This was primarily driven by robust loan growth, with loans and net leases (net of unearned income and fees) witnessing a 4.4% CAGR in the last four years ended 2023. While revenues dipped in the first quarter of 2024, decent loan demand, initiatives to boost fee income (majorly capital markets fees) and higher rates will likely aid the company’s top-line expansion.

Amid the high interest rate scenario, Zions’ net interest margin (NIM) is expected to experience a modest expansion, while rising deposit costs will weigh on it to some degree. NIM increased to 3.06% in 2022 attributed to higher rates. Though NIM declined in 2023 and the first quarter of 2024 due to higher funding costs, the metric is expected to improve in the near term, given the stabilizing deposit costs, asset yield repricing and higher rates.

Further, ZION’s capital distributions are encouraging. In 2022, the company announced an 8% increase in its quarterly dividend to 41 cents per share. Additionally, it has an existing share buyback plan. In February 2024, ZION authorized a share repurchase plan worth up to $35 million for the year. While Zions does not expect a significant amount of share buyback in the near term, the company is likely to sustain efficient capital distributions aided by a solid capital position and lower dividend payout ratio than its peers.

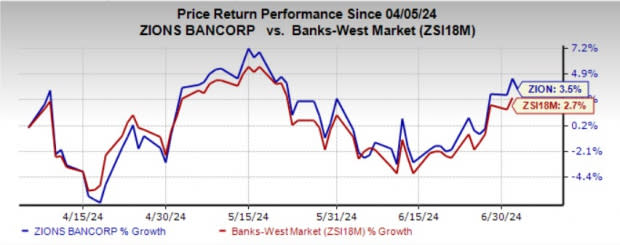

ZION currently carries a Zacks Rank #3 (Hold). In the past three months, shares of the company have gained 3.5% compared with the industry’s growth of 2.7%.

Image Source: Zacks Investment Research

Nevertheless, Zions has been witnessing a consistent rise in expenses. While total non-interest expenses decreased in 2020, the metric reflected a 4.5% CAGR in the last five years (2018-2023), primarily due to higher salary and employee benefit expenses. The uptrend persisted in the first quarter of 2024 as well. Distinctively, the company’s total technology expenditure was $483 million in 2023, which accounted for roughly 23% of total non-interest expenses. Amid its ongoing investments in franchise and digitizing operations, total expenses are expected to stay elevated in the near term.

Also, ZION’s deteriorating asset quality remains a concern. A significant rise in provision for credit losses was witnessed in 2022 and 2023. Though the metric fell in the first quarter of 2024, the current tough macroeconomic backdrop will continue to exert pressure on the company’s asset quality, thus keeping the provision levels elevated in the near term.

Banking Stocks Worth Considering

Some better-ranked banking stocks worth a look at are Northrim BanCorp, Inc. NRIM and Bank of Marin Bancorp BMRC, each sporting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks Rank #1 stocks here.

The Zacks Consensus Estimate for NRIM’s current-year earnings has been revised 12.2% upward in the past 60 days. The company’s shares have risen 17.3% in the past six months.

The Zacks Consensus Estimate for BMRC’s current-year earnings has been revised 4.8% upward in the past two months. The company’s shares have gained 6.1% in the past six months.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Zions Bancorporation, N.A. (ZION) : Free Stock Analysis Report

Northrim BanCorp Inc (NRIM) : Free Stock Analysis Report

Bank of Marin Bancorp (BMRC) : Free Stock Analysis Report