Yahoo Finance

Yahoo Finance Should You Wait Before Investing In Cohiba Minerals Limited (ASX:CHK)?

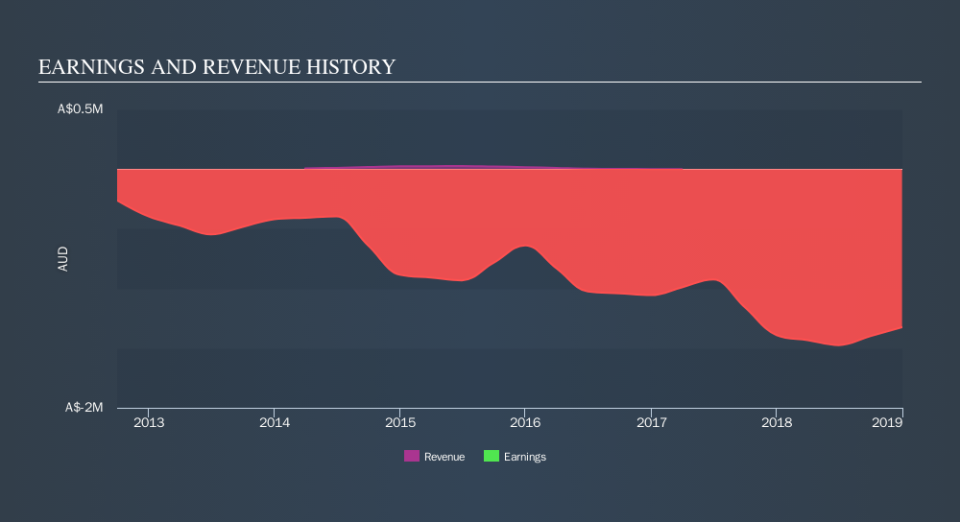

As the AU$8.6m market cap Cohiba Minerals Limited (ASX:CHK) released another year of negative earnings, investors may be on edge waiting for breakeven. The single most important question to ask when you’re investing in a loss-making company is – will it need to raise cash again, and if so, when? Cash is crucial to run a business, and if a company burns through its reserves fast, it will need to raise further funds. This may not always be on good terms, which could hurt current shareholders if the new deal lowers the value of their shares. Today I’ve examined Cohiba Minerals’s financial data from its most recent earnings update, to roughly assess when the company may need to raise new capital.

Check out our latest analysis for Cohiba Minerals

What is cash burn?

Currently, Cohiba Minerals has AU$2.4m in cash holdings and producing negative free cash flow of -AU$1.7m. The biggest threat facing Cohiba Minerals investors is the company going out of business when it runs out of money and cannot raise any more capital. Unprofitable companies operating in the highly risky metals and mining industry often face this problem, and Cohiba Minerals is no exception. The activities of these companies tend to be project-driven, which generates lumpy cash flows, meaning the business can be loss-making for a period of time while it invests heavily in a new project.

When will Cohiba Minerals need to raise more cash?

When negative, free cash flow (which I define as cash from operations minus fixed capital investment) can be an effective measure of how much Cohiba Minerals has to spend each year in order to keep its business running.

Free cash outflows declined by 29% over the past year, which could be an indication of Cohiba Minerals putting the brakes on ramping up high growth. Though, if the company kept its cash burn level at -AU$1.7m, it may not need to raise capital for another 1.4 years. Although this is a relatively simplistic calculation, and Cohiba Minerals may continue to reduce its costs further or borrow money instead of raising new equity capital, the outcome of this analysis still helps us understand how sustainable the Cohiba Minerals operation is, and when things may have to change.

Next Steps:

The risks involved in investing in loss-making Cohiba Minerals means you should think twice before diving into the stock. However, this should not prevent you from further researching it as an investment potential. The outcome of my analysis suggests that even if the company maintains this rate of cash burn growth, it will run out of cash within the year. The potential equity raising resulting from this means you might be able to get shares at a lower price if the company raises capital next. This is only a rough assessment of financial health, and CHK likely also has company-specific issues impacting its cash management decisions. You should continue to research Cohiba Minerals to get a more holistic view of the company by looking at:

Historical Performance: What has CHK's returns been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Cohiba Minerals’s board and the CEO’s back ground.

Other High-Performing Stocks: If you believe you should cushion your portfolio with something less risky, scroll through our free list of these great stocks here.

NB: Figures in this article are calculated using data from the trailing twelve months from 31 December 2018. This may not be consistent with full year annual report figures. Operating expenses include only SG&A and one-year R&D.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.