Yahoo Finance

Yahoo Finance Volatility 101: Should Mayur Resources (ASX:MRL) Shares Have Dropped 41%?

Passive investing in an index fund is a good way to ensure your own returns roughly match the overall market. While individual stocks can be big winners, plenty more fail to generate satisfactory returns. For example, the Mayur Resources Ltd (ASX:MRL) share price is down 41% in the last year. That’s disappointing when you consider the market returned 9.1%. We wouldn’t rush to judgement on Mayur Resources because we don’t have a long term history to look at. The falls have accelerated recently, with the share price down 19% in the last three months.

Check out our latest analysis for Mayur Resources

We don’t think Mayur Resources’s revenue of AU$123,290 is enough to establish significant demand. You have to wonder why venture capitalists aren’t funding it. So it seems that the investors more focused on would could be, than paying attention to the current revenues (or lack thereof). It seems likely some shareholders believe that Mayur Resources will find or develop a valuable new mine before too long.

As a general rule, if a company doesn’t have much revenue, and it loses money, then it is a high risk investment. The is usually a significant chance that they will need more money for business development, putting them at the mercy of capital markets. So the share price itself impacts the value of the shares (as it determines the cost of capital). While some such companies go on to make revenue, profits, and generate value, others get hyped up by hopeful naifs before eventually going bankrupt.

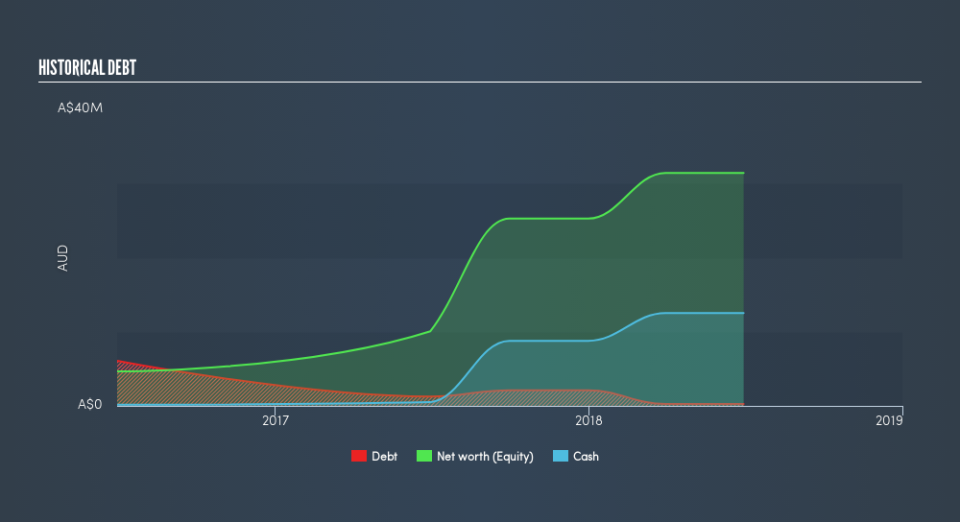

Mayur Resources had net cash of AU$8.7m when it last reported (June 2018). That’s not too bad but management may have to think about raising capital or taking on debt, unless the company is close to breaking even. With the share price down 41% in the last year, it seems likely that the need for cash is weighing on investors’ minds. The image belows shows how Mayur Resources’s balance sheet has changed over time; if you want to see the precise values, simply click on the image.

It can be extremely risky to invest in a company that doesn’t even have revenue. There’s no way to know its value easily. Would it bother you if insiders were selling the stock? It would bother me, that’s for sure. You can click here to see if there are insiders selling.

A Different Perspective

Given that the market gained 9.1% in the last year, Mayur Resources shareholders might be miffed that they lost 41%. While the aim is to do better than that, it’s worth recalling that even great long-term investments sometimes underperform for a year or more. With the stock down 19% over the last three months, the market doesn’t seem to believe that the company has solved all its problems. Basically, most investors should be wary of buying into a poor-performing stock, unless the business itself has clearly improved. Investors who like to make money usually check up on insider purchases, such as the price paid, and total amount bought. You can find out about the insider purchases of Mayur Resources by clicking this link.

Mayur Resources is not the only stock that insiders are buying. For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.