Yahoo Finance

Yahoo Finance The Urbanise.com (ASX:UBN) Share Price Has Gained 95% And Shareholders Are Hoping For More

By buying an index fund, investors can approximate the average market return. But if you buy good businesses at attractive prices, your portfolio returns could exceed the average market return. For example, Urbanise.com Limited (ASX:UBN) shareholders have seen the share price rise 95% over three years, well in excess of the market return (9.7%, not including dividends). On the other hand, the returns haven't been quite so good recently, with shareholders up just 67%.

Check out our latest analysis for Urbanise.com

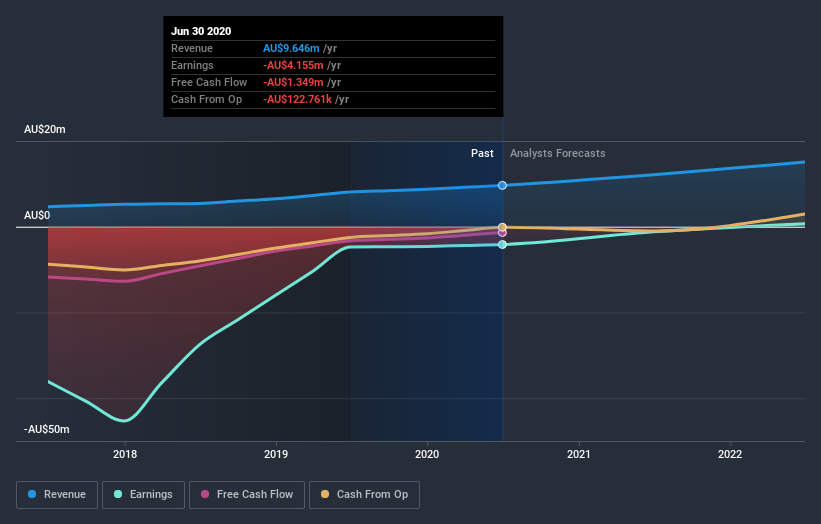

Urbanise.com isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

In the last 3 years Urbanise.com saw its revenue grow at 26% per year. That's much better than most loss-making companies. While the compound gain of 25% per year over three years is pretty good, you might argue it doesn't fully reflect the strong revenue growth. So now might be the perfect time to put Urbanise.com on your radar. If the company is trending towards profitability then it could be very interesting.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

Take a more thorough look at Urbanise.com's financial health with this free report on its balance sheet.

A Different Perspective

It's good to see that Urbanise.com has rewarded shareholders with a total shareholder return of 67% in the last twelve months. Notably the five-year annualised TSR loss of 13% per year compares very unfavourably with the recent share price performance. The long term loss makes us cautious, but the short term TSR gain certainly hints at a brighter future. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Case in point: We've spotted 3 warning signs for Urbanise.com you should be aware of.

For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.