Yahoo Finance

Yahoo Finance It's Unlikely That Lepidico Limited's (ASX:LPD) CEO Will See A Huge Pay Rise This Year

Under the guidance of CEO Joe Walsh, Lepidico Limited (ASX:LPD) has performed reasonably well recently. As shareholders go into the upcoming AGM on 22 November 2022, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders may still want to keep CEO compensation within reason.

Check out our latest analysis for Lepidico

Comparing Lepidico Limited's CEO Compensation With The Industry

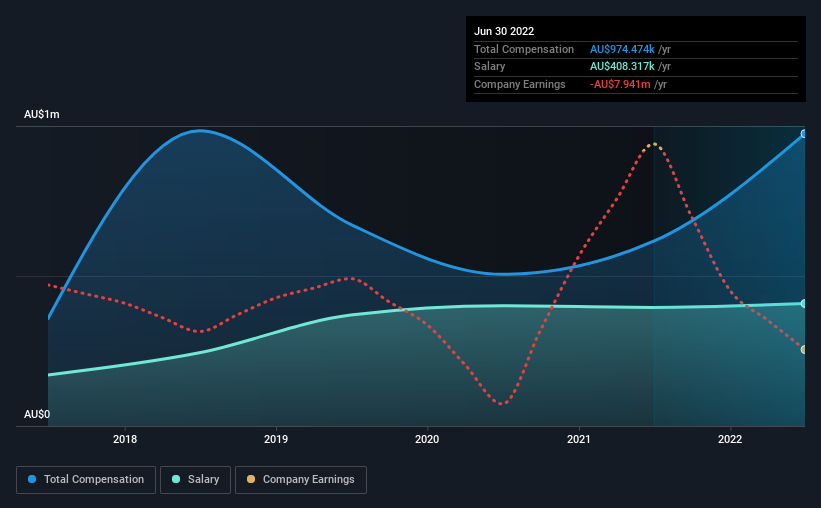

At the time of writing, our data shows that Lepidico Limited has a market capitalization of AU$145m, and reported total annual CEO compensation of AU$974k for the year to June 2022. We note that's an increase of 58% above last year. While we always look at total compensation first, our analysis shows that the salary component is less, at AU$408k.

In comparison with other companies in the industry with market capitalizations under AU$295m, the reported median total CEO compensation was AU$357k. This suggests that Joe Walsh is paid more than the median for the industry. Moreover, Joe Walsh also holds AU$707k worth of Lepidico stock directly under their own name.

Component | 2022 | 2021 | Proportion (2022) |

Salary | AU$408k | AU$395k | 42% |

Other | AU$566k | AU$221k | 58% |

Total Compensation | AU$974k | AU$616k | 100% |

Talking in terms of the industry, salary represented approximately 60% of total compensation out of all the companies we analyzed, while other remuneration made up 40% of the pie. In Lepidico's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at Lepidico Limited's Growth Numbers

Lepidico Limited has seen its earnings per share (EPS) increase by 30% a year over the past three years. It has seen most of its revenue evaporate over the past year.

This demonstrates that the company has been improving recently and is good news for the shareholders. The lack of revenue growth isn't ideal, but it is the bottom line that counts most in business. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Lepidico Limited Been A Good Investment?

With a total shareholder return of 21% over three years, Lepidico Limited shareholders would, in general, be reasonably content. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

In Summary...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

CEO pay is simply one of the many factors that need to be considered while examining business performance. That's why we did our research, and identified 4 warning signs for Lepidico (of which 2 don't sit too well with us!) that you should know about in order to have a holistic understanding of the stock.

Important note: Lepidico is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here