Yahoo Finance

Yahoo Finance Three Things You Should Check Before Buying Aurizon Holdings Limited (ASX:AZJ) For Its Dividend

Today we'll take a closer look at Aurizon Holdings Limited (ASX:AZJ) from a dividend investor's perspective. Owning a strong business and reinvesting the dividends is widely seen as an attractive way of growing your wealth. On the other hand, investors have been known to buy a stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

With a eight-year payment history and a 4.0% yield, many investors probably find Aurizon Holdings intriguing. It sure looks interesting on these metrics - but there's always more to the story . When buying stocks for their dividends, you should always run through the checks below, to see if the dividend looks sustainable.

Explore this interactive chart for our latest analysis on Aurizon Holdings!

Payout ratios

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. As a result, we should always investigate whether a company can afford its dividend, measured as a percentage of a company's net income after tax. Looking at the data, we can see that 100% of Aurizon Holdings's profits were paid out as dividends in the last 12 months. With a payout ratio this high, we'd say its dividend is not well covered by earnings. This may be fine if earnings are growing, but it might not take much of a downturn for the dividend to come under pressure.

Another important check we do is to see if the free cash flow generated is sufficient to pay the dividend. Aurizon Holdings paid out 58% of its free cash flow last year, which is acceptable, but is starting to limit the amount of earnings that can be reinvested into the business. It's good to see that while Aurizon Holdings's dividends were not covered by profits, at least they are affordable from a cash perspective. Still, if the company repeatedly paid a dividend greater than its profits, we'd be concerned. Very few companies are able to sustainably pay dividends larger than their reported earnings.

Is Aurizon Holdings's Balance Sheet Risky?

As Aurizon Holdings's dividend was not well covered by earnings, we need to check its balance sheet for signs of financial distress. A rough way to check this is with these two simple ratios: a) net debt divided by EBITDA (earnings before interest, tax, depreciation and amortisation), and b) net interest cover. Net debt to EBITDA is a measure of a company's total debt. Net interest cover measures the ability to meet interest payments. Essentially we check that a) the company does not have too much debt, and b) that it can afford to pay the interest. With net debt of 2.39 times its EBITDA, Aurizon Holdings has a noticeable amount of debt, although if business stays steady, this may not be overly concerning.

We calculated its interest cover by measuring its earnings before interest and tax (EBIT), and dividing this by the company's net interest expense. Aurizon Holdings has EBIT of 5.82 times its interest expense, which we think is adequate.

Consider getting our latest analysis on Aurizon Holdings's financial position here.

Dividend Volatility

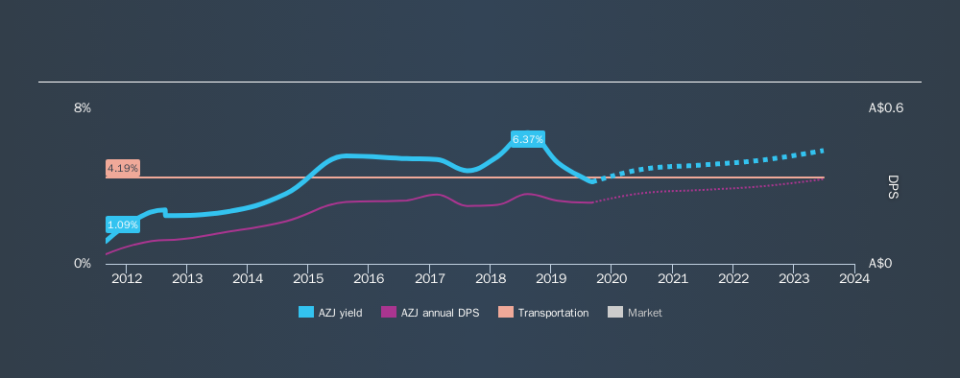

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. Looking at the last decade of data, we can see that Aurizon Holdings paid its first dividend at least eight years ago. It's good to see that Aurizon Holdings has been paying a dividend for a number of years. However, the dividend has been cut at least once in the past, and we're concerned that what has been cut once, could be cut again. During the past eight-year period, the first annual payment was AU$0.037 in 2011, compared to AU$0.24 last year. This works out to be a compound annual growth rate (CAGR) of approximately 26% a year over that time. The growth in dividends has not been linear, but the CAGR is a decent approximation of the rate of change over this time frame.

Aurizon Holdings has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, but it might be worth considering if the business has turned a corner.

Dividend Growth Potential

With a relatively unstable dividend, it's even more important to see if earnings per share (EPS) are growing. Why take the risk of a dividend getting cut, unless there's a good chance of bigger dividends in future? It's good to see Aurizon Holdings has been growing its earnings per share at 15% a year over the past 5 years. While EPS are growing rapidly, Aurizon Holdings paid out a very high 100% of its income as dividends. If earnings continue to grow, this dividend may be sustainable, but we think a payout this high definitely bears watching.

Conclusion

To summarise, shareholders should always check that Aurizon Holdings's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. We're not keen on the fact that Aurizon Holdings paid out such a high percentage of its income, although its cashflow is in better shape. Unfortunately, the company has not been able to generate earnings per share growth, and cut its dividend at least once in the past. While we're not hugely bearish on it, overall we think there are potentially better dividend stocks than Aurizon Holdings out there.

Companies that are growing earnings tend to be the best dividend stocks over the long term. See what the 9 analysts we track are forecasting for Aurizon Holdings for free with public analyst estimates for the company.

We have also put together a list of global stocks with a market capitalisation above $1bn and yielding more 3%.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.