Yahoo Finance

Yahoo Finance We Think Solid State (LON:SOLI) Can Stay On Top Of Its Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Solid State plc (LON:SOLI) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Solid State

What Is Solid State's Debt?

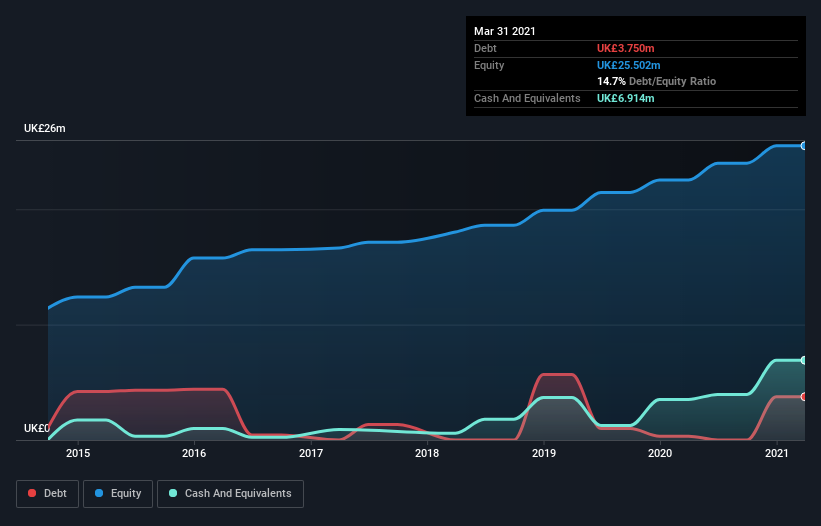

The image below, which you can click on for greater detail, shows that at March 2021 Solid State had debt of UK£3.75m, up from UK£333.0k in one year. But it also has UK£6.91m in cash to offset that, meaning it has UK£3.16m net cash.

A Look At Solid State's Liabilities

According to the last reported balance sheet, Solid State had liabilities of UK£15.7m due within 12 months, and liabilities of UK£12.7m due beyond 12 months. Offsetting this, it had UK£6.91m in cash and UK£11.8m in receivables that were due within 12 months. So it has liabilities totalling UK£9.71m more than its cash and near-term receivables, combined.

Since publicly traded Solid State shares are worth a total of UK£85.1m, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, Solid State boasts net cash, so it's fair to say it does not have a heavy debt load!

But the other side of the story is that Solid State saw its EBIT decline by 5.2% over the last year. If earnings continue to decline at that rate the company may have increasing difficulty managing its debt load. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Solid State's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Solid State has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Solid State actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

While Solid State does have more liabilities than liquid assets, it also has net cash of UK£3.16m. And it impressed us with free cash flow of UK£5.8m, being 142% of its EBIT. So is Solid State's debt a risk? It doesn't seem so to us. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Solid State's earnings per share history for free.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.