Yahoo Finance

Yahoo Finance We Think Shareholders Will Probably Be Generous With Frontier Developments plc's (LON:FDEV) CEO Compensation

It would be hard to discount the role that CEO David Braben has played in delivering the impressive results at Frontier Developments plc (LON:FDEV) recently. The pleasing results would be something shareholders would keep in mind at the upcoming AGM on 27 October 2021. The focus will probably be on the future company strategy as shareholders cast their votes on resolutions such as executive remuneration and other matters. We think the CEO has done a pretty decent job and we discuss why the CEO compensation is appropriate.

View our latest analysis for Frontier Developments

How Does Total Compensation For David Braben Compare With Other Companies In The Industry?

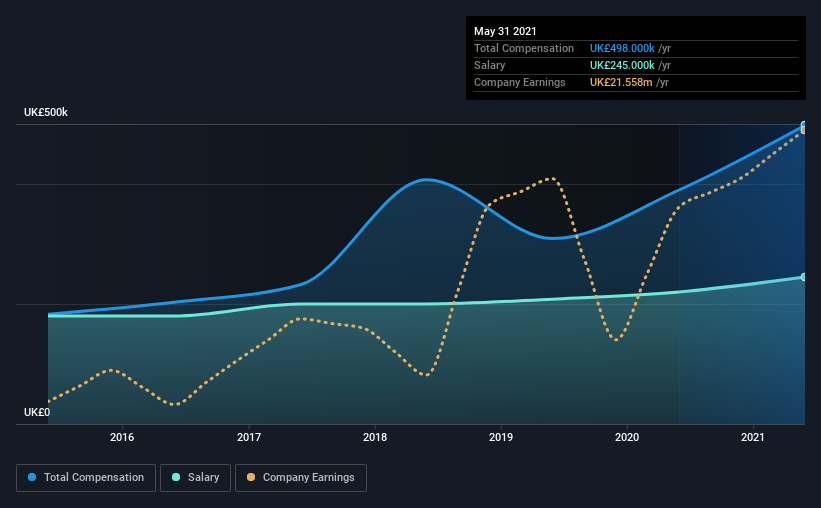

At the time of writing, our data shows that Frontier Developments plc has a market capitalization of UK£1.0b, and reported total annual CEO compensation of UK£498k for the year to May 2021. We note that's an increase of 28% above last year. We think total compensation is more important but our data shows that the CEO salary is lower, at UK£245k.

On comparing similar companies from the same industry with market caps ranging from UK£723m to UK£2.3b, we found that the median CEO total compensation was UK£534k. This suggests that Frontier Developments remunerates its CEO largely in line with the industry average. What's more, David Braben holds UK£344m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

Component | 2021 | 2020 | Proportion (2021) |

Salary | UK£245k | UK£220k | 49% |

Other | UK£253k | UK£170k | 51% |

Total Compensation | UK£498k | UK£390k | 100% |

On an industry level, roughly 70% of total compensation represents salary and 30% is other remuneration. It's interesting to note that Frontier Developments allocates a smaller portion of compensation to salary in comparison to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

Frontier Developments plc's Growth

Frontier Developments plc has seen its earnings per share (EPS) increase by 79% a year over the past three years. It achieved revenue growth of 19% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's a real positive to see this sort of revenue growth in a single year. That suggests a healthy and growing business. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Frontier Developments plc Been A Good Investment?

Most shareholders would probably be pleased with Frontier Developments plc for providing a total return of 152% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

The company's solid performance might have made most shareholders happy, possibly making CEO remuneration the least of the matters to be discussed in the AGM. However, investors will get the chance to engage on key strategic initiatives and future growth opportunities for the company and set their longer-term expectations.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. That's why we did our research, and identified 2 warning signs for Frontier Developments (of which 1 is a bit concerning!) that you should know about in order to have a holistic understanding of the stock.

Switching gears from Frontier Developments, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.