Yahoo Finance

Yahoo Finance We Think Artemis Resources (ASX:ARV) Needs To Drive Business Growth Carefully

We can readily understand why investors are attracted to unprofitable companies. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

Given this risk, we thought we'd take a look at whether Artemis Resources (ASX:ARV) shareholders should be worried about its cash burn. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

View our latest analysis for Artemis Resources

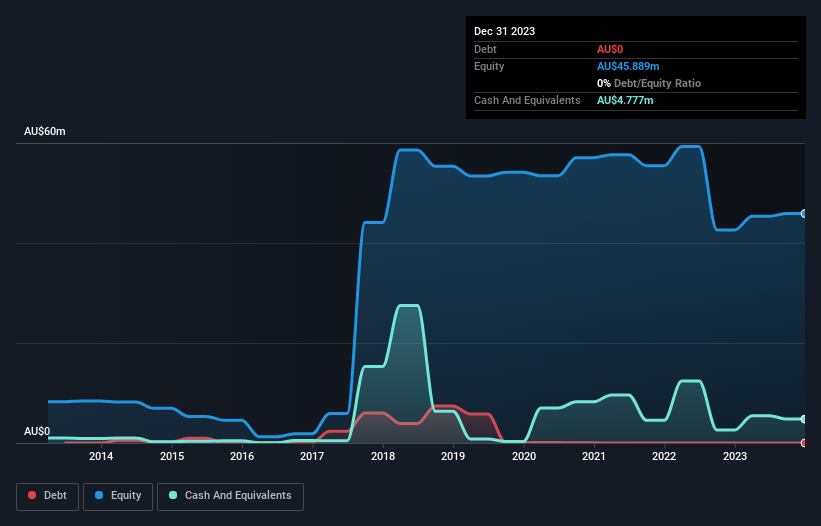

Does Artemis Resources Have A Long Cash Runway?

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. When Artemis Resources last reported its December 2023 balance sheet in March 2024, it had zero debt and cash worth AU$4.8m. Looking at the last year, the company burnt through AU$4.5m. So it had a cash runway of approximately 13 months from December 2023. While that cash runway isn't too concerning, sensible holders would be peering into the distance, and considering what happens if the company runs out of cash. You can see how its cash balance has changed over time in the image below.

How Is Artemis Resources' Cash Burn Changing Over Time?

Whilst it's great to see that Artemis Resources has already begun generating revenue from operations, last year it only produced AU$80k, so we don't think it is generating significant revenue, at this point. As a result, we think it's a bit early to focus on the revenue growth, so we'll limit ourselves to looking at how the cash burn is changing over time. The 64% reduction in its cash burn over the last twelve months may be good for protecting the balance sheet but it hardly points to imminent growth. Artemis Resources makes us a little nervous due to its lack of substantial operating revenue. We prefer most of the stocks on this list of stocks that analysts expect to grow.

How Hard Would It Be For Artemis Resources To Raise More Cash For Growth?

There's no doubt Artemis Resources' rapidly reducing cash burn brings comfort, but even if it's only hypothetical, it's always worth asking how easily it could raise more money to fund further growth. Companies can raise capital through either debt or equity. Commonly, a business will sell new shares in itself to raise cash and drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Artemis Resources has a market capitalisation of AU$32m and burnt through AU$4.5m last year, which is 14% of the company's market value. Given that situation, it's fair to say the company wouldn't have much trouble raising more cash for growth, but shareholders would be somewhat diluted.

Is Artemis Resources' Cash Burn A Worry?

Artemis Resources appears to be in pretty good health when it comes to its cash burn situation. Not only was its cash burn relative to its market cap quite good, but its cash burn reduction was a real positive. While we're the kind of investors who are always a bit concerned about the risks involved with cash burning companies, the metrics we have discussed in this article leave us relatively comfortable about Artemis Resources' situation. On another note, we conducted an in-depth investigation of the company, and identified 6 warning signs for Artemis Resources (4 make us uncomfortable!) that you should be aware of before investing here.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.