Yahoo Finance

Yahoo Finance Stock Market: The Earnings of Microsoft, Amazon And More

Ford Motor

EPS forecast: $0.26

Revenue forecast: $36.73B

Ford has been going through a hard time during the past few years as the demand for its cars, particularly sedans, fell. Now one of America’s largest automakers is undertaking an $11 billion restructuring plan which implies layoffs, closing factories overseas, and building capacity to manufacture electric and driverless cars. As a result, investors will want to see what progress the company made in these areas.

The stock has been within the general downtrend since 2014. In the first half of 2019, the price tried to recover but met resistance around $10.50, formed a double top and turned lower. In October, Ford managed to show a bullish correction recovering from $8.45 to the 200-day MA at $9.30. Last week the stock closed above the 50-week MA ($9.214). All in all, if the financial results are decent enough, there’s technical potential for an extension to $9.64 (September high) and $10.00 (resistance line, 200-week MA). This area, in turn, will be a great obstacle for buyers. Support lies at $8.70 and $8.45.

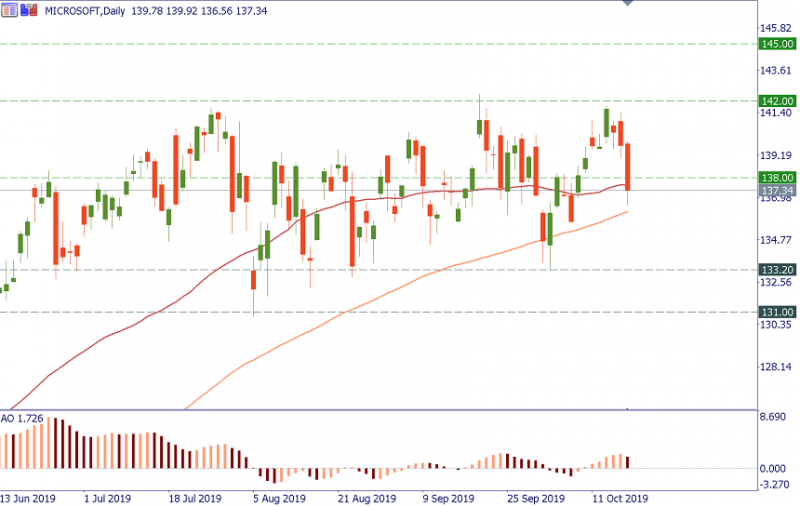

Microsoft

EPS forecast: $1.24

Revenue forecast: $32.14B

According to analysts’ forecasts, Microsoft’s earnings will rise by 9%, while revenue will increase by 10.5% y/y. Noticed that during previous quarters, the company tended to beat expectations. Microsoft has a variety of products that generate solid income. Pay special attention to the dynamics of Azure, its cloud computing service – the figures should once again be pretty impressive as the tech giant added new capabilities to its product.

The stock has been trading sideways between $142 and $131 since the end of June. The price consolidated after a long-term uptrend. Currently, it’s in the $137 area, near the middle of the horizontal range. Its edges, mentioned earlier, are the initial targets.

Tesla

EPS forecast: $-0.45

Revenue forecast: $6.47B

Tesla is expected to show the third unprofitable quarter in a row despite selling a record number of cars. At this point, bad figures will be a surprise to no one, so investors, on the contrary, will look for glimpses of light: a forecast for future profit, a positive free cash flow, evidence that demand remains solid. If the electric vehicle maker doesn’t provide these sources of hope, the negative pressure on the stock will mount.

After the selloff in the first half of the year, Tesla bottomed in June and then managed to stabilize. Most recently, the price met the resistance of the July high ($266). On the upside, there are also obstacles at $268 and $273.6 (50- and 200-period MAs) ahead of $278 (50% Fibo retracement of the 2018-2019 decline). Support lies at $235 and $231 (daily MAs) as well as $225 (support line).

eBay

EPS forecast: $0.64

Revenue forecast: $2.65B

Analysts have positive expectations about eBay’s financial results. The company’s putting a lot of effort into the technological enhancement of its core e-commerce business. On the downside, the increased investment may hurt earnings. In addition, notice that the competition with Amazon and Wal-Mart is a big challenge for eBay. Investors will also look for the news regarding the potential sale of StubHub or eBay Classifieds, a contentious issue for the company that provoked the departure of its CEO last month.

The stock has been on the rise since the end of 2018. However, at the end of September, the price slipped below $39 – this level tends to be an important border for eBay during the whole year. A return above $39.50 (100- and 50-day MAs) is needed to open the way up to $41 and 42.50 (78.6% Fibo retracement of the 2018 decline). Support is at 37.65 (200-day MA), $36.50 and $35.50.

Thursday, October 24

Amazon.com

EPS forecast: $4.59

Revenue forecast: $68.82B

According to Wall Street, Amazon’s adjusted earnings will decline by about 20% y/y showing the first decline in nine quarters. The company’s revenue, however, is seen increasing by 22%. During the last few months, Amazon was pressured by lower-than-expected earnings, volatile equity markets, political criticism, and antitrust allegations. In this report, investors will look at the numbers for Amazon Web Services (the company’s cloud segment), the signs that the Prime delivery speed increase is boosting sales growth in North America as well as Amazon’s guidance for the next quarter.

Although Amazon remains one of the best long-term performers among both tech and consumer goods stocks, it is behind other the other so-called FAANG stocks during the past year. In August, the stock violated the uptrend from the end of 2018. The price then started trading below $1,835/50, limited by the 100- and the 50-day MAs. The most recent attempt of the price to get higher ran into an obstacle just below $1,800, near the 200-day MA. All the mentioned levels will act as resistance. Below $1,740 support is at $1,700 and $1,670 (June low).

Intel

EPS forecast: $1.23

Revenue forecast: $18.02B

During the previous quarter, Intel benefited from rising demand for personal computers and sales of higher-priced server chips. Investors will want to see whether the positive trend continues and what the semiconductor producer projects for the rest of the year. So far, the stock has been resilient enough despite the trade war between the United States and China, an important market for the chipmaker, although the threat of higher tariffs has obviously limited its upside.

The stock of Intel is trading within an ascending triangle. The resistance that has been keeping the price from getting higher lies at $53.20 (61.8% Fibo retracement of the April-May decline). The break above this obstacle will open the way up to $55 and $56 (78.6% Fibo). Support lies at $50 (200-day MA, support line) and $49.20/00. The loss of 48.50 will make the price vulnerable for a decline to $46.75.

Visa

EPS forecast: $1.43

Revenue forecast: $6.08B

For years, Visa’s stock has been slowly but surely appreciating – a reflection of the fact that digital payment is replacing cash. This tendency has all the chances to continue pushing the price higher, although there may be corrections on the way. This time, Wall Street sees Visa earnings rising by 18% y/y and revenue grows at 12%. Notice that Visa has a tendency to beat forecasts during the earnings releases.

Visa’s long-term uptrend ran in September into the resistance at $187.00. Since then, the price has consolidated around $175.00. The further resistance is at $190 and $200. On the downside, support lies at $169.00 and $163.80 (200-day MA). The fall below $160 will question the uptrend.

This article was originally posted on FX Empire

More From FXEMPIRE:

AUD/USD Price Forecast – Australian Dollar Runs Into Resistance

Futures Flat After McDonald’s Miss, Brexit Votes Expected Today, Trade Hopes Fuel Optimism

Natural Gas Price Prediction – Prices Rebound Near Support On Colder Weather Forecast

Crude Oil Price Update – Holding Above $52.94 Will Generate Upside Bias