Yahoo Finance

Yahoo Finance Read This Before Buying Vita Group Limited (ASX:VTG) For Its Dividend

Could Vita Group Limited (ASX:VTG) be an attractive dividend share to own for the long haul? Investors are often drawn to strong companies with the idea of reinvesting the dividends. Unfortunately, it's common for investors to be enticed in by the seemingly attractive yield, and lose money when the company has to cut its dividend payments.

In this case, Vita Group likely looks attractive to dividend investors, given its 7.9% dividend yield and nine-year payment history. We'd agree the yield does look enticing. There are a few simple ways to reduce the risks of buying Vita Group for its dividend, and we'll go through these below.

Click the interactive chart for our full dividend analysis

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. So we need to form a view on if a company's dividend is sustainable, relative to its net profit after tax. Vita Group paid out 61% of its profit as dividends, over the trailing twelve month period. This is a healthy payout ratio, and while it does limit the amount of earnings that can be reinvested in the business, there is also some room to lift the payout ratio over time.

Another important check we do is to see if the free cash flow generated is sufficient to pay the dividend. The company paid out 71% of its free cash flow, which is not bad per se, but does start to limit the amount of cash Vita Group has available to meet other needs. It's positive to see that Vita Group's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

With a strong net cash balance, Vita Group investors may not have much to worry about in the near term from a dividend perspective.

We update our data on Vita Group every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility

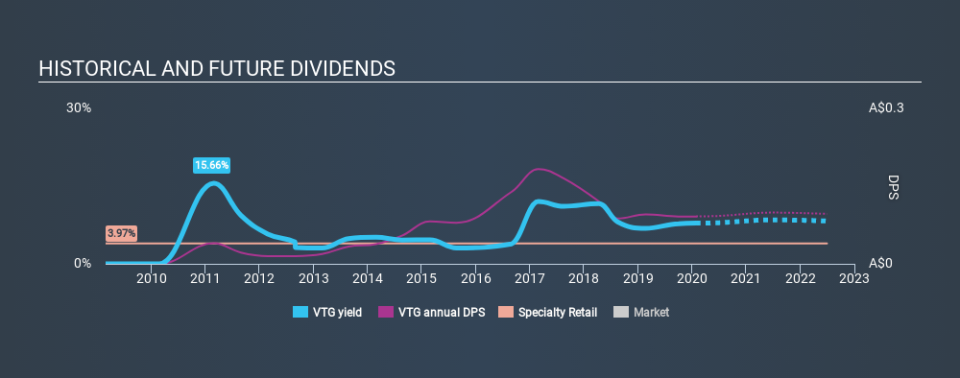

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. Looking at the last decade of data, we can see that Vita Group paid its first dividend at least nine years ago. It's good to see that Vita Group has been paying a dividend for a number of years. However, the dividend has been cut at least once in the past, and we're concerned that what has been cut once, could be cut again. During the past nine-year period, the first annual payment was AU$0.04 in 2011, compared to AU$0.092 last year. This works out to be a compound annual growth rate (CAGR) of approximately 9.7% a year over that time. Vita Group's dividend payments have fluctuated, so it hasn't grown 9.7% every year, but the CAGR is a useful rule of thumb for approximating the historical growth.

Dividends have grown at a reasonable rate, but with at least one substantial cut in the payments, we're not certain this dividend stock would be ideal for someone intending to live on the income.

Dividend Growth Potential

With a relatively unstable dividend, it's even more important to see if earnings per share (EPS) are growing. Why take the risk of a dividend getting cut, unless there's a good chance of bigger dividends in future? Earnings have grown at around 4.8% a year for the past five years, which is better than seeing them shrink! Growth of 4.8% is relatively anaemic growth, which we wonder about. If the company is struggling to grow, perhaps that's why it elects to pay out more than half of its earnings to shareholders.

We'd also point out that Vita Group issued a meaningful number of new shares in the past year. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

Conclusion

When we look at a dividend stock, we need to form a judgement on whether the dividend will grow, if the company is able to maintain it in a wide range of economic circumstances, and if the dividend payout is sustainable. Vita Group's is paying out more than half its income as dividends, but at least the dividend is covered by both reported earnings and cashflow. Second, earnings growth has been ordinary, and its history of dividend payments is chequered - having cut its dividend at least once in the past. In sum, we find it hard to get excited about Vita Group from a dividend perspective. It's not that we think it's a bad business; just that there are other companies that perform better on these criteria.

You can also discover whether shareholders are aligned with insider interests by checking our visualisation of insider shareholdings and trades in Vita Group stock.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.