Yahoo Finance

Yahoo Finance A Quick Analysis On RedFlow's (ASX:RFX) CEO Compensation

Tim Harris became the CEO of RedFlow Limited (ASX:RFX) in 2018, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

Check out our latest analysis for RedFlow

Comparing RedFlow Limited's CEO Compensation With the industry

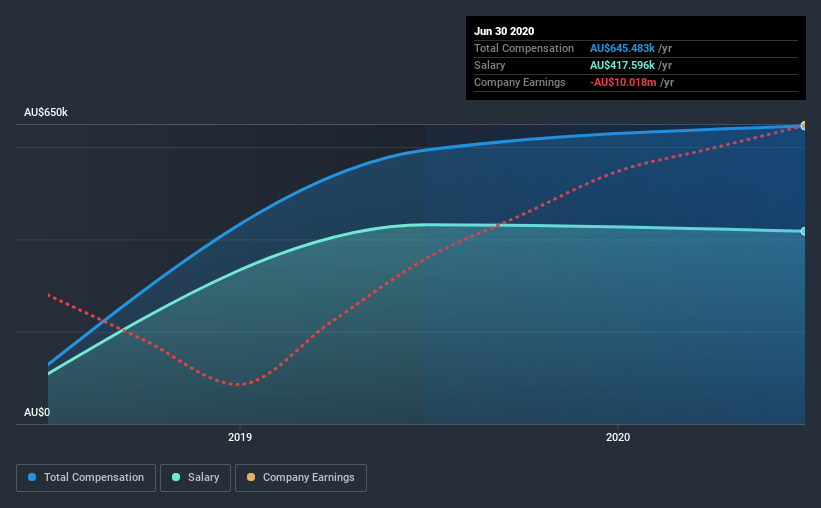

According to our data, RedFlow Limited has a market capitalization of AU$31m, and paid its CEO total annual compensation worth AU$645k over the year to June 2020. That's a notable increase of 8.8% on last year. We note that the salary portion, which stands at AU$417.6k constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the industry with market capitalizations under AU$272m, the reported median total CEO compensation was AU$213k. Hence, we can conclude that Tim Harris is remunerated higher than the industry median. Furthermore, Tim Harris directly owns AU$69k worth of shares in the company.

Component | 2020 | 2019 | Proportion (2020) |

Salary | AU$418k | AU$432k | 65% |

Other | AU$228k | AU$162k | 35% |

Total Compensation | AU$645k | AU$593k | 100% |

On an industry level, around 70% of total compensation represents salary and 30% is other remuneration. Our data reveals that RedFlow allocates salary more or less in line with the wider market. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at RedFlow Limited's Growth Numbers

RedFlow Limited has seen its earnings per share (EPS) increase by 34% a year over the past three years. Its revenue is up 151% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. The combination of strong revenue growth with medium-term EPS improvement certainly points to the kind of growth we like to see. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has RedFlow Limited Been A Good Investment?

Given the total shareholder loss of 78% over three years, many shareholders in RedFlow Limited are probably rather dissatisfied, to say the least. So shareholders would probably want the company to be lessto generous with CEO compensation.

To Conclude...

As we noted earlier, RedFlow pays its CEO higher than the norm for similar-sized companies belonging to the same industry. However, the EPS growth is certainly impressive, but we cannot say the same about the uninspiring shareholder returns (over the last three years). Considering overall performance, we can't say Tim is underpaid, in fact compensation is definitely on the higher side.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. That's why we did our research, and identified 5 warning signs for RedFlow (of which 1 is a bit concerning!) that you should know about in order to have a holistic understanding of the stock.

Switching gears from RedFlow, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.