Yahoo Finance

Yahoo Finance Positive earnings growth hasn't been enough to get Carrier Global (NYSE:CARR) shareholders a favorable return over the last year

The simplest way to benefit from a rising market is to buy an index fund. While individual stocks can be big winners, plenty more fail to generate satisfactory returns. For example, the Carrier Global Corporation (NYSE:CARR) share price is down 23% in the last year. That falls noticeably short of the market decline of around 17%. We wouldn't rush to judgement on Carrier Global because we don't have a long term history to look at. The falls have accelerated recently, with the share price down 22% in the last three months. However, one could argue that the price has been influenced by the general market, which is down 15% in the same timeframe.

The recent uptick of 5.5% could be a positive sign of things to come, so let's take a lot at historical fundamentals.

See our latest analysis for Carrier Global

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

During the unfortunate twelve months during which the Carrier Global share price fell, it actually saw its earnings per share (EPS) improve by 18%. It could be that the share price was previously over-hyped.

It's surprising to see the share price fall so much, despite the improved EPS. So it's well worth checking out some other metrics, too.

Given the yield is quite low, at 1.7%, we doubt the dividend can shed much light on the share price. Carrier Global's revenue is actually up 13% over the last year. Since the fundamental metrics don't readily explain the share price drop, there might be an opportunity if the market has overreacted.

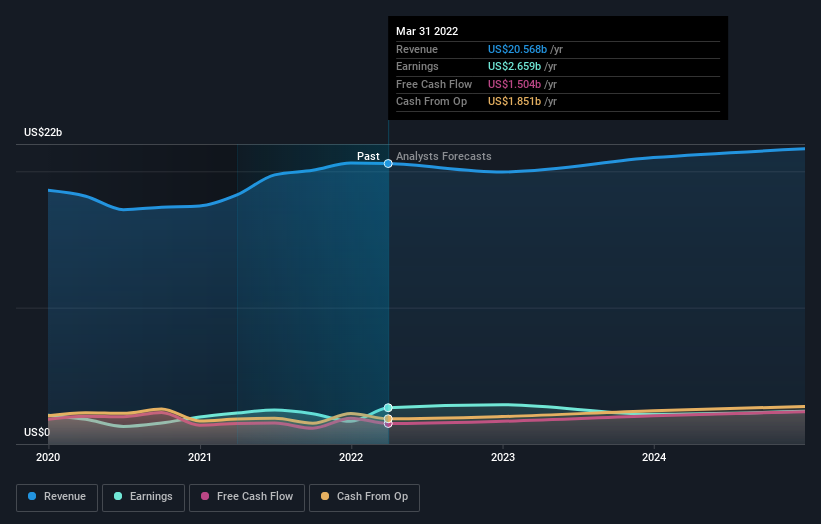

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

Carrier Global is well known by investors, and plenty of clever analysts have tried to predict the future profit levels. So we recommend checking out this free report showing consensus forecasts

A Different Perspective

We doubt Carrier Global shareholders are happy with the loss of 22% over twelve months (even including dividends). That falls short of the market, which lost 17%. There's no doubt that's a disappointment, but the stock may well have fared better in a stronger market. The share price decline has continued throughout the most recent three months, down 22%, suggesting an absence of enthusiasm from investors. Given the relatively short history of this stock, we'd remain pretty wary until we see some strong business performance. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For example, we've discovered 5 warning signs for Carrier Global (1 is potentially serious!) that you should be aware of before investing here.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.