Yahoo Finance

Yahoo Finance Pentamaster International (HKG:1665) Seems To Use Debt Rather Sparingly

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Pentamaster International Limited (HKG:1665) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Pentamaster International

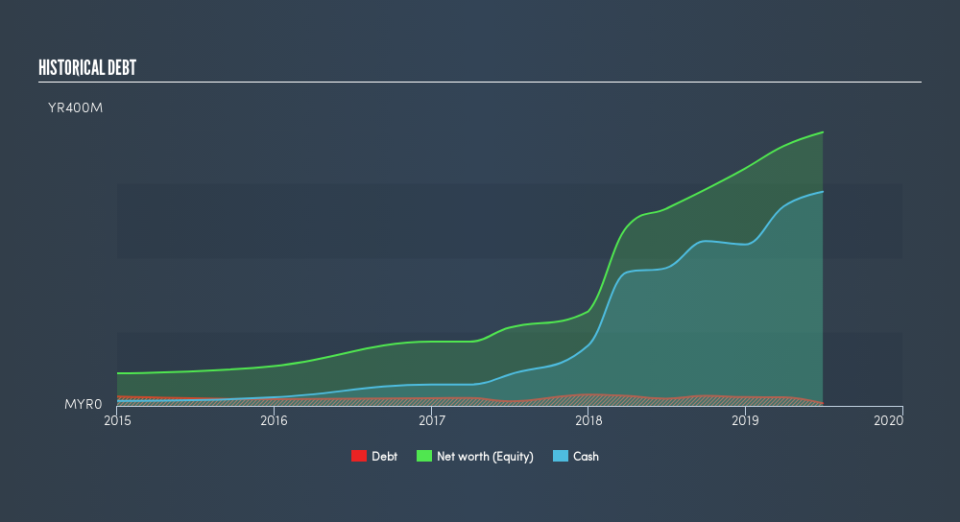

How Much Debt Does Pentamaster International Carry?

As you can see below, Pentamaster International had RM3.50m of debt at June 2019, down from RM9.89m a year prior. But on the other hand it also has RM289.1m in cash, leading to a RM285.6m net cash position.

A Look At Pentamaster International's Liabilities

Zooming in on the latest balance sheet data, we can see that Pentamaster International had liabilities of RM171.1m due within 12 months and liabilities of RM131.0k due beyond that. On the other hand, it had cash of RM289.1m and RM56.4m worth of receivables due within a year. So it actually has RM174.2m more liquid assets than total liabilities.

This short term liquidity is a sign that Pentamaster International could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, Pentamaster International boasts net cash, so it's fair to say it does not have a heavy debt load!

Even more impressive was the fact that Pentamaster International grew its EBIT by 111% over twelve months. That boost will make it even easier to pay down debt going forward. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Pentamaster International can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Pentamaster International has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Pentamaster International generated free cash flow amounting to a very robust 85% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Summing up

While it is always sensible to investigate a company's debt, in this case Pentamaster International has RM286m in net cash and a decent-looking balance sheet. And it impressed us with free cash flow of RM106m, being 85% of its EBIT. So is Pentamaster International's debt a risk? It doesn't seem so to us. We'd be very excited to see if Pentamaster International insiders have been snapping up shares. If you are too, then click on this link right now to take a (free) peek at our list of reported insider transactions.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.