Yahoo Finance

Yahoo Finance MYTHBUSTER: ‘Investing ethically gets you worse returns’

With 55 per cent of all Australian assets under management now incorporating environmental, social and governance (ESG) considerations, ethical investing has in fact become the new normal.

Only last week, the world’s largest asset manager said sustainable investing will be core to how everyone invests in the future, and that assets in ETFs that incorporate these ‘ESG’ factors will grow from US$25 billion (AU$35 billion) to more than US$400 billion (AU$566 billion) in a decade.

But not all investors were on board from the get-go, doubtful that returns can keep pace with mainstream investment vehicles.

However, a swag of reports and studies prove otherwise.

This myth of needing to trade off financial returns for social and environmental impact is a particular bug-bear of Giant Leap Fund managing partner Will Richardson.

“Investors have often struggled with the idea that they can make money and do good at the same time,” said Simon O’Connor, the Responsible Investment Association Australasia (RIAA) CEO.

“However the figures are beginning to paint a different story, showing the strong performance of responsible investments.”

Unconvinced? We’ll let the numbers do the talking. We’ve rounded up a number of studies, charts, research, facts and figures that empirically debunk the myth, once and for all.

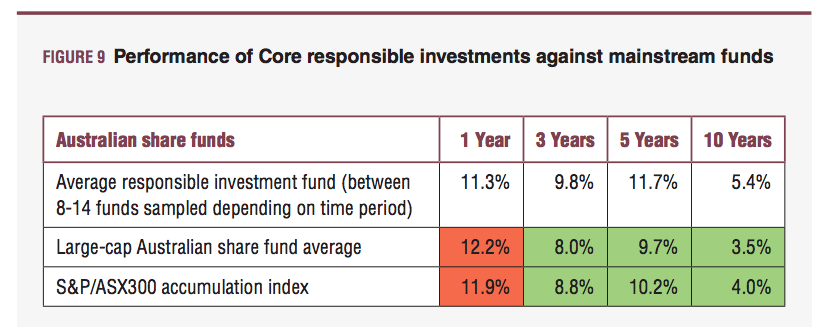

Mythbuster 1. “Core responsible investment Australian share funds outperformed large-cap Australian share funds”

Arguably the authority in Australia’s responsible investing landscape, RIAA’s latest benchmark report finds that Australian responsible investment funds overperformed on a three-year, five-year and ten-year basis.

Mythbuster 2. “Firms with good ratings on material sustainability issues significantly outperform firms with poor ratings”

Published three years ago, this Harvard study is oft-cited. Academics from these American universities sought to provide new evidence around “the value implications of sustainability investments”.

The result? “…we find that firms with good ratings on material sustainability issues significantly outperform firms with poor ratings on these issues.”

Source: Harvard Business School, the University of Minnesota, and Northwestern University – ‘Corporate Sustainability: First Evidence on Materiality’

Mythbuster 3. “90% of studies find a nonnegative ESG–CFP relation”

This mammoth meta-study is no joke, pulling stats from over 2000 studies about the impact of ESG factors on financial performance.

“This study examines the entire universe of ESG-[corporate financial performance] academic review studies that have been published since 1970,” the report states.

“Roughly 90% of studies find a nonnegative ESG–CFP relation. More importantly, the large majority of studies report positive findings.”

Not only that, but some asset classes proved the link between ESG and performance quite strongly, particularly bonds and real estate.

Thankfully, a more snackable breakdown of the report findings is available.

Mythbuster 4, 5, 6 & 7. “Can socially responsible investing and good returns coexist? Spoiler alert: the answer is yes.”

Their cheeky sub-heading just about sums it up. Much like this article, Morphic’s compact report presents the findings of a number of studies detailed below that debunk the “misconception” that “you can’t have your cake and eat it too.”

In January 2017, UBS Asset Management’s head of sustainable and impact investing Michael Baldinger made the case for why incorporating sustainability metrics “is no longer just a nice-to-have”.

“The team at UBS Quantitative Research has examined a number of recent studies to determine whether ESG investment bias in portfolios produces better returns,” Baldinger wrote.

“They found that while it is sometimes statistically insignificant, investment strategies that screen for ESG criteria on average outperform those that do not.”

Then there’s this study from the University of Brussel, Harvard University and Arabesque Partners that tested whether fund managers would be disadvantaged by managing a portfolio with some ESG screens applied to it.

“For three out of the four universes we have created, ESG screening not only does not hurt performance, but actually improves risk-adjusted returns,” the report said.

“The findings of our study suggest that a preliminary ESG screening can make sense for any investment strategy, even when there is no specific goal to address sustainability.

“That is to say, instead of starting with an unscreened universe, an ESG filter can effectively create a universe of stocks with improved risk-return characteristics and diversification.”

And finally, this research report from Santa Clara University’s Meir Statman and the University of Pennsylvania’s Denys Glushkov came to an interesting conclusion.

Where portfolios were more heavily tilted towards stocks with better social responsibility characteristics, they outperformed conventional portfolios; but once negative screening was also applied, the returns were offset such that the net effect was ‘no effect’.

The conclusion was an approach that did both. “That method calls for tilts toward stocks of companies with high social responsibility scores on such characteristics as community, employee relations, and the environment, but it also calls for refraining from shunning the stocks of any company.”

Ultimately, the decision of where you put your money lies with you alone. However, with countless more examples of studies proving you can do good with your investments, it’s getting harder and harder to deny the cold hard facts.

Make your money work with Yahoo Finance’s daily newsletter. Sign up here and stay on top of the latest money, news and tech news.