Yahoo Finance

Yahoo Finance How Much Is Orthocell Limited (ASX:OCC) CEO Getting Paid?

The CEO of Orthocell Limited (ASX:OCC) is Paul Anderson, and this article examines the executive's compensation against the backdrop of overall company performance. This analysis will also assess whether Orthocell pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

See our latest analysis for Orthocell

How Does Total Compensation For Paul Anderson Compare With Other Companies In The Industry?

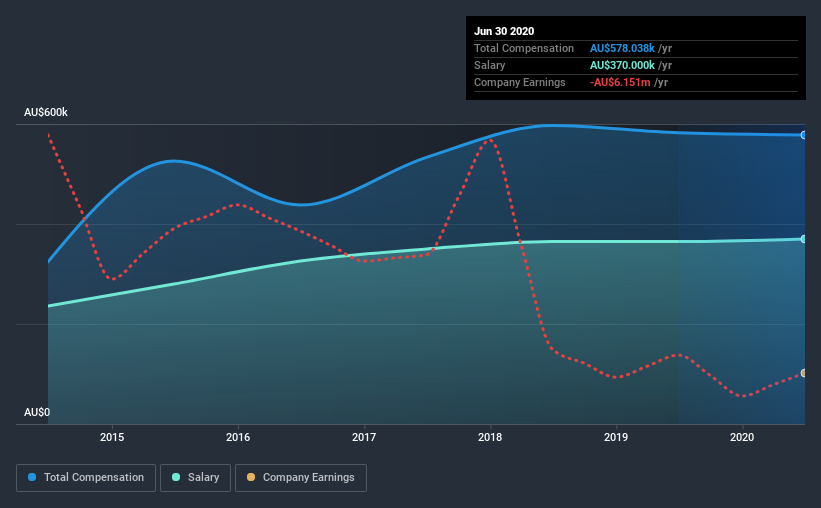

At the time of writing, our data shows that Orthocell Limited has a market capitalization of AU$75m, and reported total annual CEO compensation of AU$578k for the year to June 2020. That is, the compensation was roughly the same as last year. In particular, the salary of AU$370.0k, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the industry with market capitalizations below AU$276m, reported a median total CEO compensation of AU$432k. Accordingly, our analysis reveals that Orthocell Limited pays Paul Anderson north of the industry median. What's more, Paul Anderson holds AU$1.4m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

Component | 2020 | 2019 | Proportion (2020) |

Salary | AU$370k | AU$365k | 64% |

Other | AU$208k | AU$217k | 36% |

Total Compensation | AU$578k | AU$582k | 100% |

On an industry level, around 67% of total compensation represents salary and 33% is other remuneration. Our data reveals that Orthocell allocates salary more or less in line with the wider market. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Orthocell Limited's Growth Numbers

Over the last three years, Orthocell Limited has shrunk its earnings per share by 5.1% per year. Its revenue is down 24% over the previous year.

Overall this is not a very positive result for shareholders. And the impression is worse when you consider revenue is down year-on-year. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Orthocell Limited Been A Good Investment?

Orthocell Limited has served shareholders reasonably well, with a total return of 21% over three years. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

As previously discussed, Paul is compensated more than what is normal for CEOs of companies of similar size, and which belong to the same industry. This doesn't look great when you realize that the company has been suffering from negative EPS growth for the last three years. And shareholder returns are decent but not great. So you may want to delve deeper, because we don't think the amount Paul makes is justifiable.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. That's why we did our research, and identified 4 warning signs for Orthocell (of which 2 are potentially serious!) that you should know about in order to have a holistic understanding of the stock.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.