Yahoo Finance

Yahoo Finance How Much Did Anglo American's (LON:AAL) CEO Pocket Last Year?

This article will reflect on the compensation paid to Mark Cutifani who has served as CEO of Anglo American plc (LON:AAL) since 2013. This analysis will also look to assess whether the CEO is appropriately paid, considering recent earnings growth and investor returns for Anglo American.

View our latest analysis for Anglo American

Comparing Anglo American plc's CEO Compensation With the industry

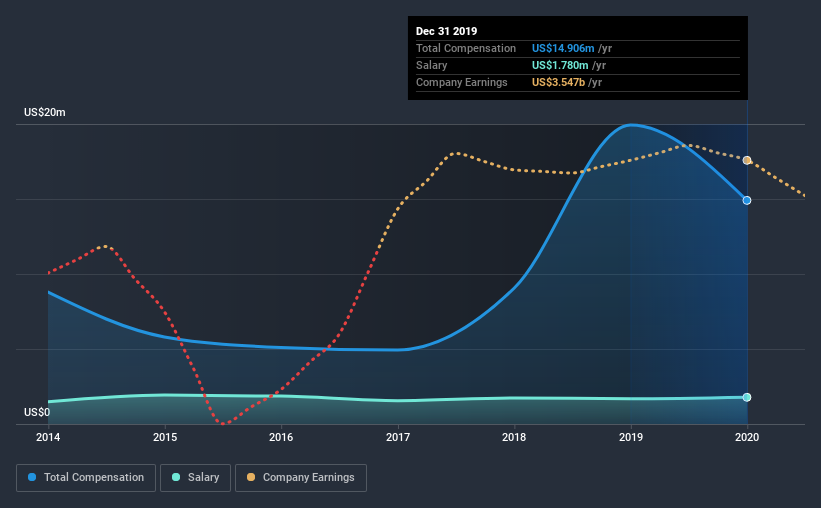

Our data indicates that Anglo American plc has a market capitalization of UK£23b, and total annual CEO compensation was reported as UK£15m for the year to December 2019. We note that's a decrease of 25% compared to last year. We think total compensation is more important but our data shows that the CEO salary is lower, at UK£1.8m.

For comparison, other companies in the industry with market capitalizations above UK£6.2b, reported a median total CEO compensation of UK£1.6m. Accordingly, our analysis reveals that Anglo American plc pays Mark Cutifani north of the industry median. Moreover, Mark Cutifani also holds UK£19m worth of Anglo American stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

Component | 2019 | 2018 | Proportion (2019) |

Salary | UK£1.8m | UK£1.7m | 12% |

Other | UK£13m | UK£18m | 88% |

Total Compensation | UK£15m | UK£20m | 100% |

On an industry level, around 64% of total compensation represents salary and 36% is other remuneration. Anglo American pays a modest slice of remuneration through salary, as compared to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

Anglo American plc's Growth

Anglo American plc has reduced its earnings per share by 17% a year over the last three years. Its revenue is down 3.9% over the previous year.

Few shareholders would be pleased to read that EPS have declined. And the impression is worse when you consider revenue is down year-on-year. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Anglo American plc Been A Good Investment?

Most shareholders would probably be pleased with Anglo American plc for providing a total return of 48% over three years. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

As we noted earlier, Anglo American pays its CEO higher than the norm for similar-sized companies belonging to the same industry. The company isn't growing EPS, but shareholder returns have been impressive over the last three years. Considering positive investor returns, it would be bold of us to criticize CEO compensation, but shareholders might want to see healthier EPS growth before a raise is given out.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 3 warning signs for Anglo American that investors should think about before committing capital to this stock.

Important note: Anglo American is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.